There are effectively three kinds of SaaS and it seems the (public) markets can’t tell the difference between the three with the coming AI wave.

Group 1: Software utility is not tied to heads, or if tied to heads not based on those heads delivering an outcome WITH the software. Companies can’t cut back on Workday seats because of AI! Quickbooks is used in small businesses. These systems of record will add AI features which will be accretive to revenue — think background checks for Workday, collections for QuickBooks, etc.

Group 2: AI potentially lowers # of users of the product but potentially introduces more usage? If you need fewer graphics designers you might need less Adobe licenses, but it’s possible you need more? Or the expanded output and productivity gains of AI increases usage?

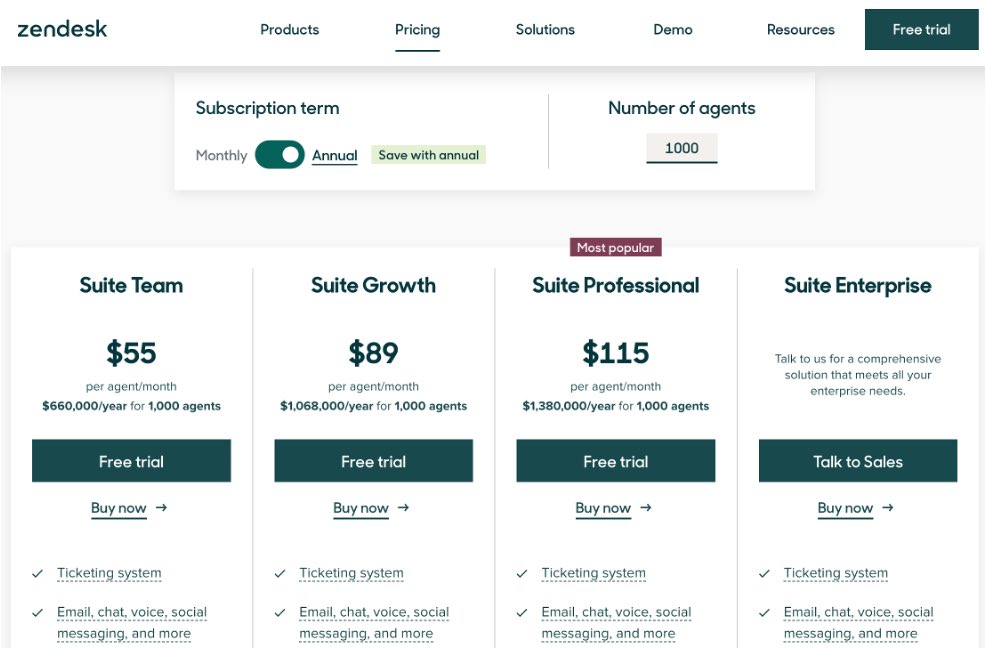

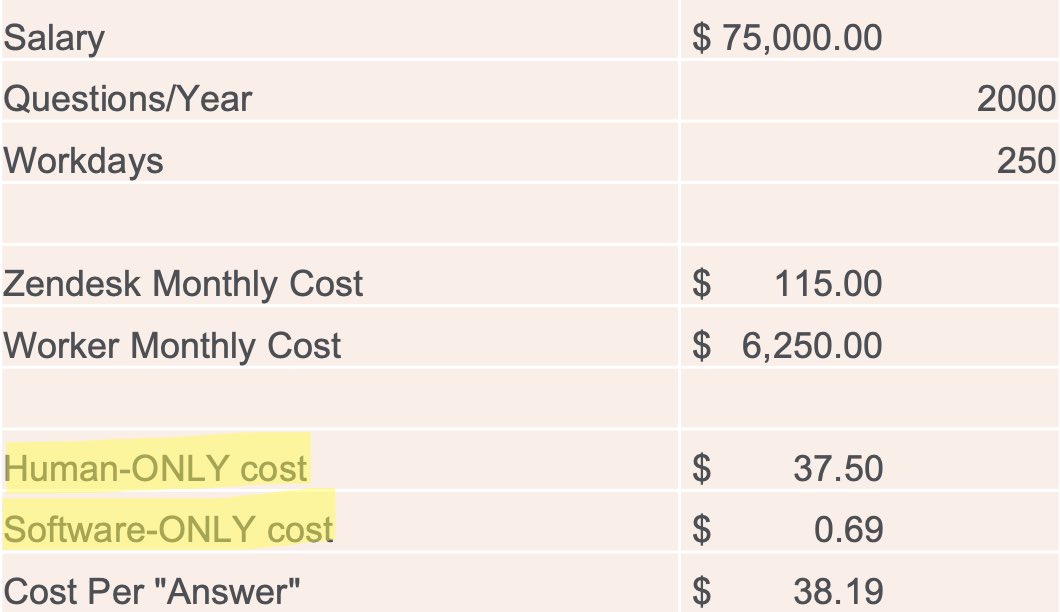

Group 3: Software utility and pricing are DIRECTLY based on heads using software, where AI directly erases heads for the vertical. Zendesk falls squarely in this category. Theoretically CRM could, too. Without a pivot to outcome based pricing, these guys are in trouble.

But there’s a huge difference between the three. The best companies often have hostages, not customers — and they will maintain pricing irrespective of AI usage.

There’s another thread of “companies will vibe code their own software” but unlikely for critical systems of record where renting is cheaper than owning (hence the shift to SaaS from On Prem starting 20 years ago!)

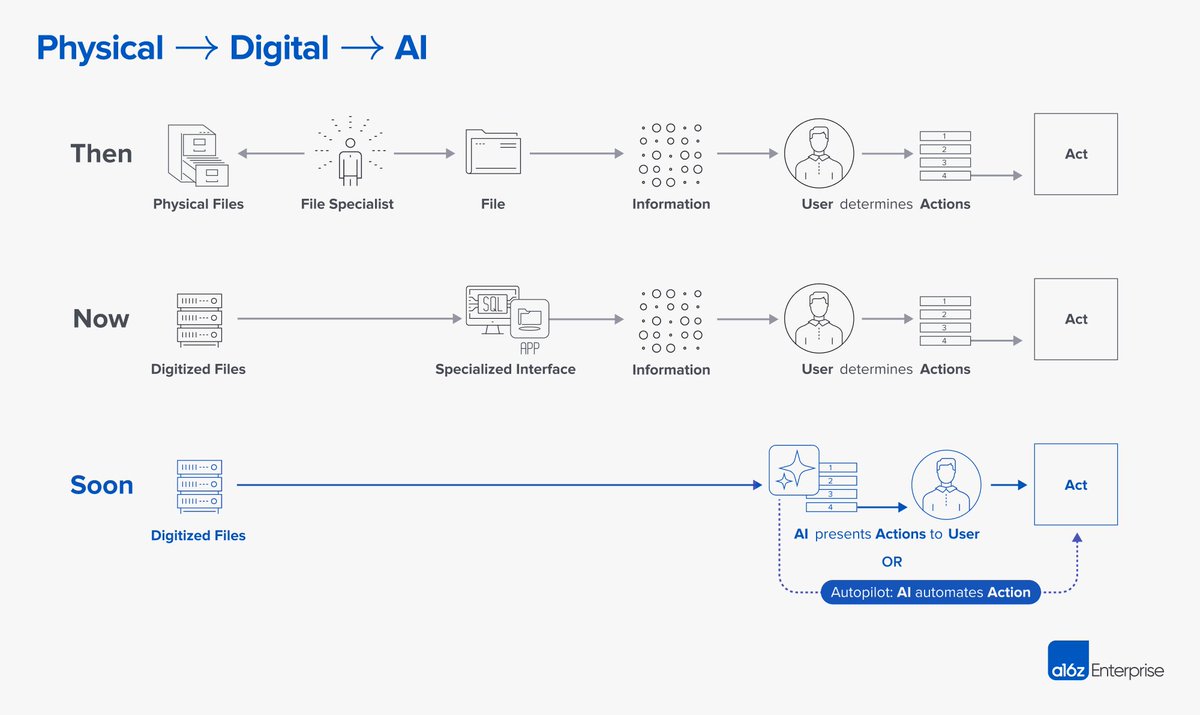

More here on the value of filing cabinets: