Originally posted as a Twitter thread on September 18, 2019

September 18th marks the 61st anniversary of the most valuable network effect of all time: the credit card. How did we get here? Read on. And read @opinion_joe ‘s book “Piece of the Action” for more…

The epicenter of the revolution was Fresno, California. Facebook started with the contained network of Harvard students; the humble credit card started with 60,000 people in Fresno and a prominent company called Bank of America, then a California-only bank.

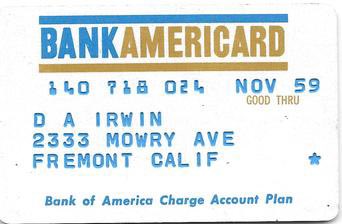

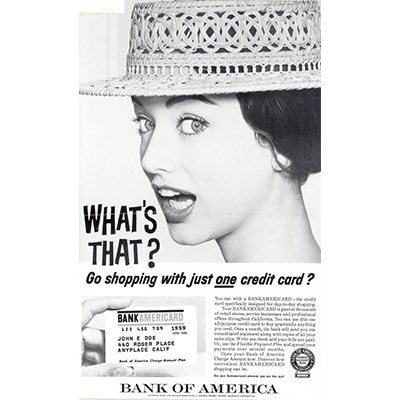

There was no application. 60,000 people just got a BankAmericard in the mail on September 18, 1958, ready to use.

There were “charge cards” like Diner’s Club before the BankAmericard Fresno drop, but there was no “credit” being extended. And you could go to a bank and get a loan, or get an installment loan for a specific purchase, but in person.

The credit card came out of Bank of America’s corporate think tank, called the “Customer Services Research Department,” run by a 41 year old man named Joe Williams.

Consumers were used to paying on credit, but each line of credit was either specific to a merchant (e.g., Sears), or a burdensome process requiring a new loan (in person) from the bank.

Williams thought the credit card — a multi-merchant product — would fix that. It really had two purposes: convenience and lending.

Fresno at the time had about 250,000 people, and *45% of all Fresno families* were Bank of America customers.

Credit card fees were set at 6% for merchants, and consumers — who just randomly got this card without applying — got between $300 and $500 in instant credit.

The brilliance of the 60,000 person drop is that Williams had effectively started with the chicken, in the classic chicken/egg cold start problem. On day 1, cardholders simply *existed* which permitted BoA to sign up all merchants who didn’t have existing proprietary programs

So Williams started in a seemingly random, highly concentrated town, immediately enlisted existing customers, and focused on fast-moving, small merchants — not the giants like Sears — all backed by a massive advertising campaign.

More than 300 merchants in the city signed up, the first being Florsheim Shoes (still around!).

Within 3 months, BoA was expanding concentrically — to Modesto to the north and Bakersfield to the south, and within a year San Francisco, Sacramento, and Los Angeles. Within 13 months of Fresno, there were 2 million cards issued and 20,000 merchants onboarded.

After the Fresno drop, other banks followed. Chase Manhattan was 5 months later on the east coast.

Williams assumed that collections would be a breeze, that late payments would never cross 4%, and that existing bank credit systems would work. Instead, less than 2 years after Fresno, Joe Williams quit BoA due to a series of disasters. The credit card almost died then+there

Delinquencies were over 20%. Fraud was out of control as criminals figured out how to replicate cards. Merchants (harbinger of things to come) hated paying 6% and the first battles over fees began. Some of them stole from the bank or customers, too.

And more broadly — and this is now illegal — simply giving people cards without having them apply, and without them understanding the consequences of wanton spending, created far more bad debt than BoA had ever seen (on a customer % basis).

The huge losses and mounting pressure almost caused BoA to kill the card program altogether. The founder was ousted. Instead, BoA persevered, and just a few years later BankAmericard turned a profit and grew like a rocketship, transforming how people pay and borrow.

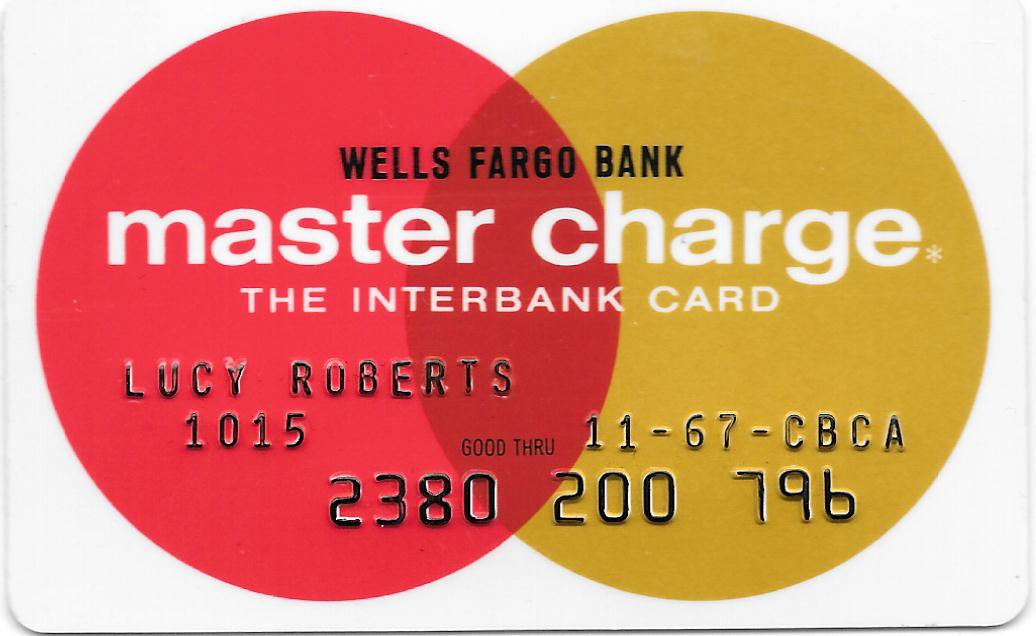

Eventually, BankAmericard became a non-profit consortium called Visa — uniting many banks with competing credit cards. A competing consortium called MasterCharge, later MasterCard, did the same with another set of banks.

Credit cards and payment cards are arguably the most valuable network in the world, with at least $1T of publicly traded market cap (Visa, MasterCard, the banks who issue them, etc)…all starting off in a little town called Fresno, on a random day in September of 1958.

More on how credit cards work today and their history:

And how all of this — and the creation of this powerful network effect — has an impact on how I think about crypto (old tweetstorm from last year): https://x.com/arampell/status/1042226753253437440?s=21

FIN