Originally posted as a Twitter thread on September 27, 2021

There have been many attempts to topple payment network effects by paying users to switch. This almost never works, because (a) more people are motivated by convenience than small amounts of money, and (b) those motivated by money will suck up all the promotional budget ASAP

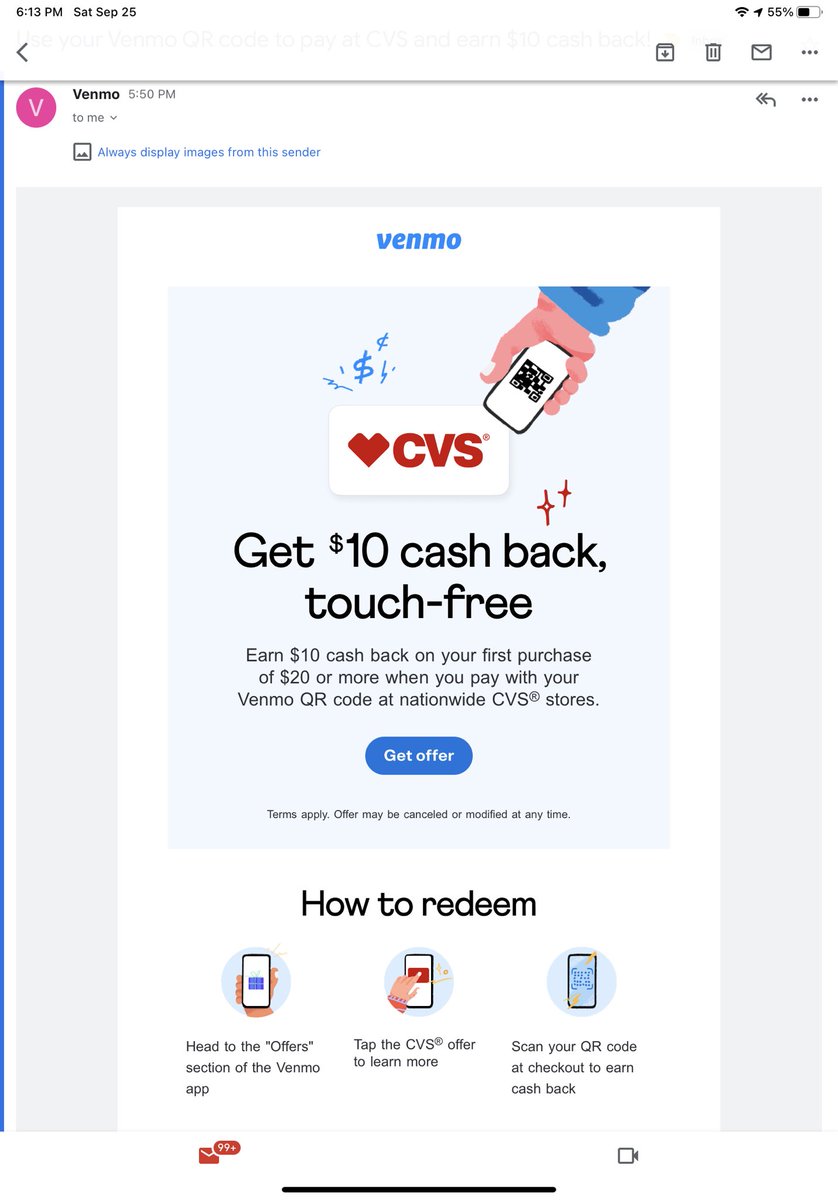

Good case study today is here, with Venmo, straight to my inbox. $10 of $20 at CVS! CVS doesn’t have 50% gross margins, so Venmo is almost certainly paying. But will “normal” people use this? Will it change behavior in a lasting way?

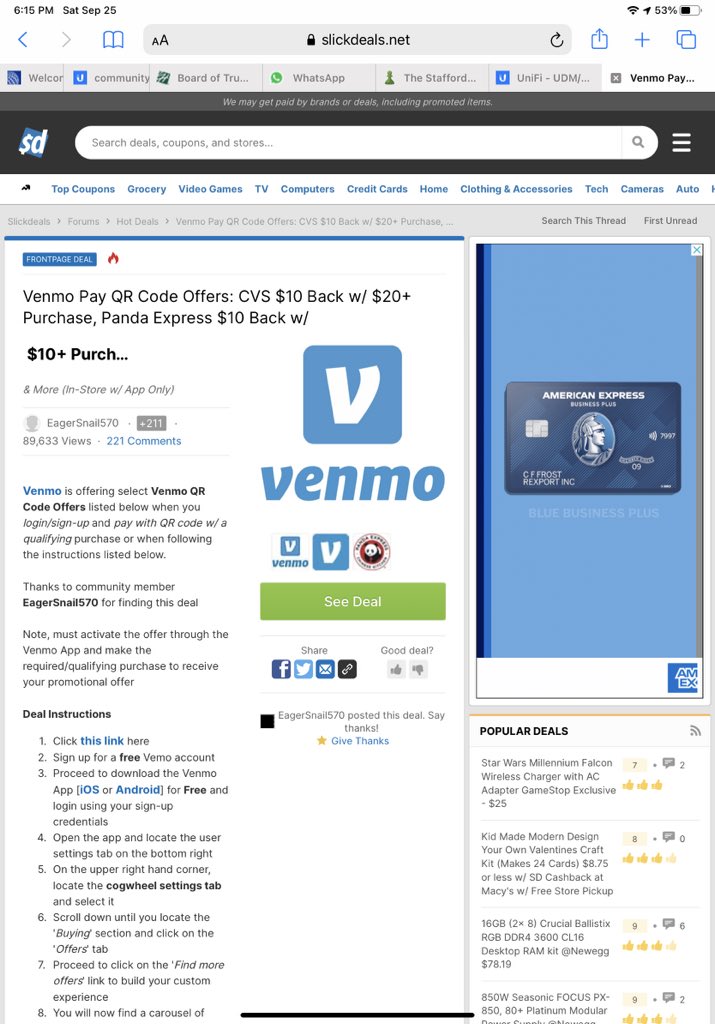

Whenever a promotion like this happens, the “deal hunters” of the internet rejoice! You can even buy a $20 CVS gift card for $10 + sell it on eBay for $15! See here, on Slickdeals…the promotion is capped (100M people can’t use it, that would be $1B!) and gets quickly depleted

PayPal did this with HomeDepot in 2012, in an attempt to jumpstart their offline business. https://www.wsj.com/articles/SB10001424052970203513604577145140658342670

Promotions aplenty (50% off etc), but it didn’t work…at least not in changing behavior. People (the deal seeking people!) pillaged the promotions and moved on.

A good rule of thumb: a new technology will take off “automatically” if it’s 10x better and 1/10th the cost. Payments offline just work, hard to make them 10x better (vs online, where many opportunities since people don’t memorize their credentials…lots of abandoned carts)

So then there’s cost, where you generate merchant excitement with anything that’s 1/10th the cost, but then fail to persuade consumers to adopt it since they lose their rewards. I often describe interchange as a problem of concentrated benefit (banks/V/MA) and diffuse costs…

Saving 2% on your $5 purchase is simply not compelling enough to sign up for a new payment instrument, or switch payment instruments, even though repeated enough times it’s real money. And the merchant might simply try to keep the savings, versus pass on to consumers.

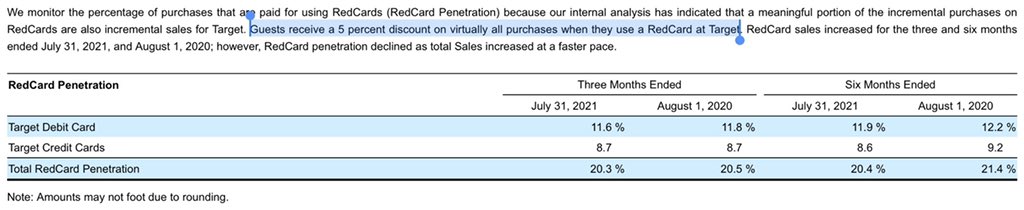

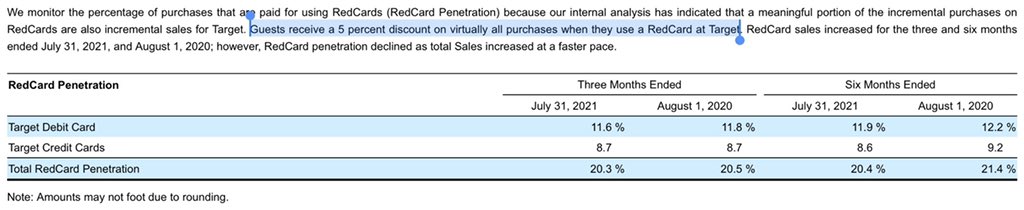

Look at Target. ~$25B in sales, if this were all credit @ ~2% (it’s not) that would be $500M in fees, or a 20% bump to operating income if they eliminated it. Target has something called their RedCard, which now accounts for >20% of sales by…providing 5% (!!) discounts

So Target *did* switch 20% of people over, which is impressive — but would those people stick if the 5% rebate went away? Maybe…but probably not? (NB: Target made $172M last quarter in a profit sharing agreement with TD for the Target Credit Card)

It *is* valuable to become (and pay for) the default payment in a new wallet with repeat usage that’s “set it and forget it.” Uber, Starbucks, United, Amazon…all have “wallets” with stored value, and credentials, that could theoretically be used elsewhere (e.g., AmazonPay).

The reason I find BNPL interesting is, as I stated here, the ability to produce a parallel network that yields more sales and customer utilization “organically”:

https://x.com/arampell/status/1435692945387048964?s=21 https://x.com/arampell/status/1435692945387048964

Changing behavior is tough, and providing discounts and offers generally doesn’t generate the lasting behavior change companies want. Google learned this lesson with Google Checkout, Visa with Visa Checkout, MasterCard with MasterPass, etc.

13/ So the opportunities and questions are: can you *in a lasting way* appeal to convenience vs cost? If so, a one-time incentive *might* be just fine. Otherwise — it’s probably wasted ammunition against the impenetrable fortress of interchange.