Originally posted as a Twitter thread on October 17, 2022

How we almost merged our company TrialPay, many times, while navigating the “can’t raise cash without growth, can’t grow without raising cash” problem. The embedded thread shows the surviving path, but let me walk you through several that *didn’t* work https://x.com/arampell/status/1562557849128931328

It’s not uncommon during bull markets to have too many competitors on the field for a given space. A “roll-up” can theoretically create more pricing power while eliminating redundant teams, tech platforms, etc…increasing revenue while lowering OpEx! “Synergies” galore 🏦💵

And even without an “over-competed” space, you might have one company with LOTS of cash, and another with lots of product-market fit but unable to raise…so one way to “raise money” is effectively to just merge with a cash-rich competitor. If cash is king, merge with cash!

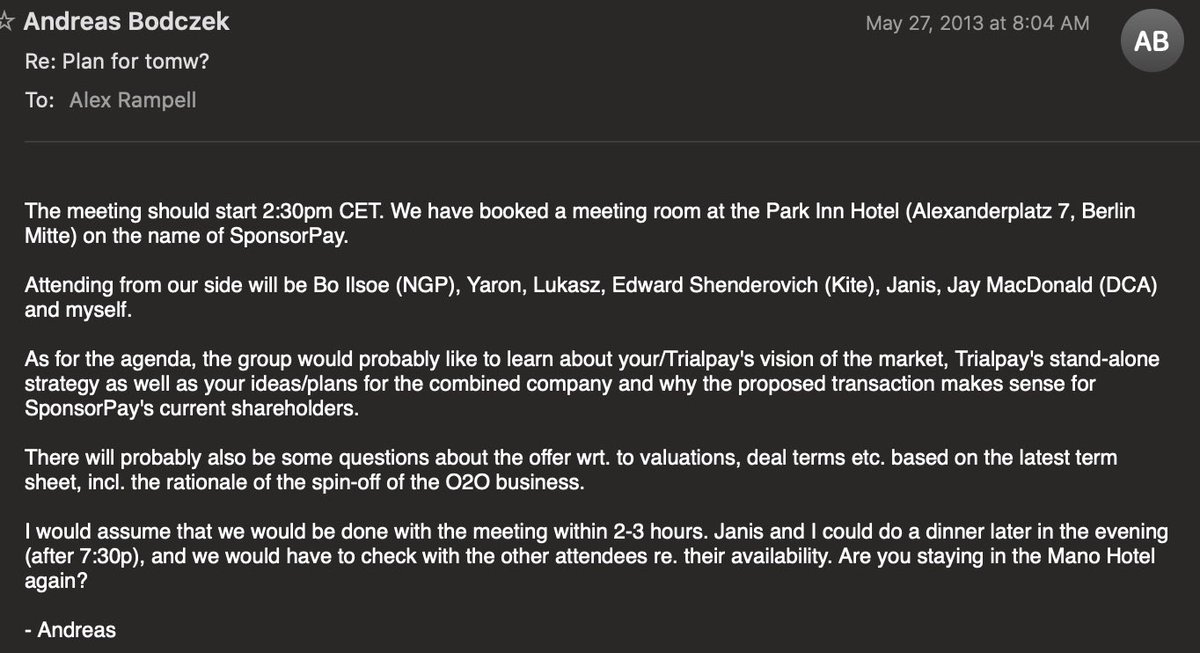

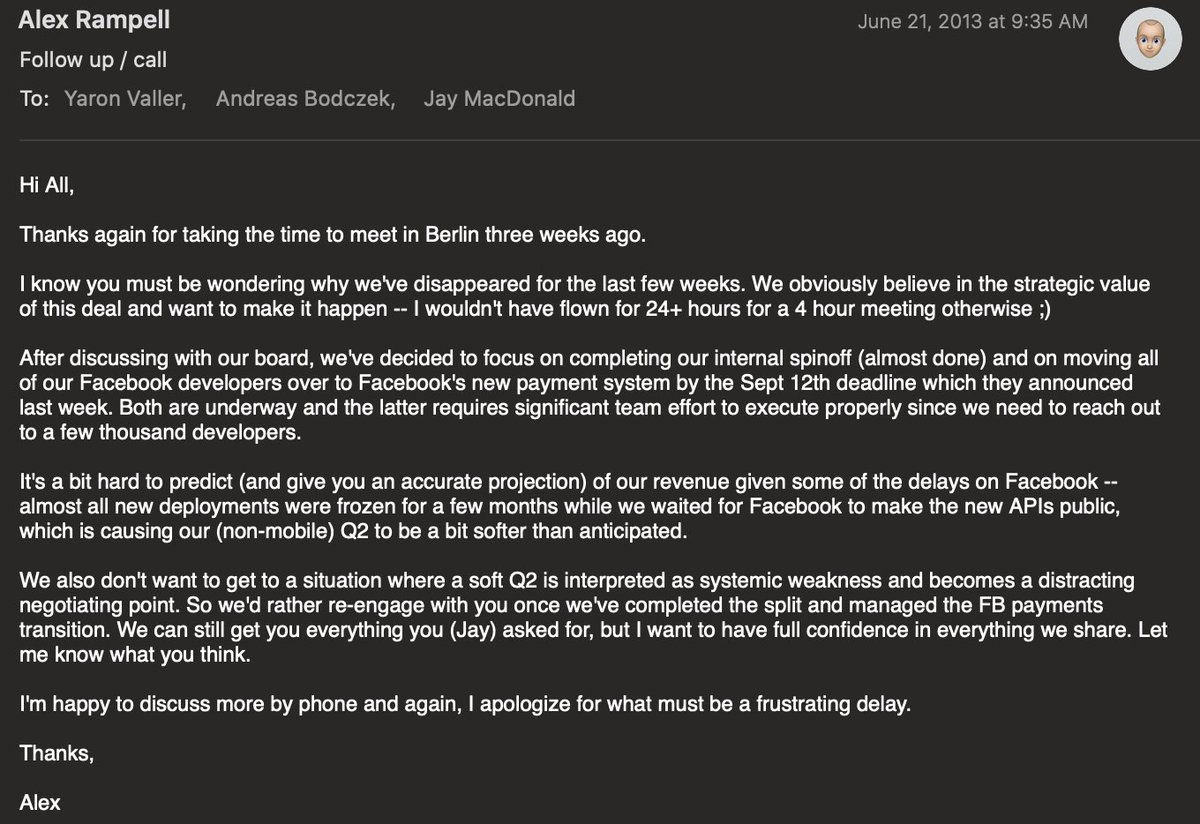

Let’s go back to May 28, 2013. Here I am in the *last* row of the now defunct AirBerlin, flying from LAX to Berlin to meet with SponsorPay regarding a merger. I needed to make a presentation and proposal, which I attempted to do from my seat…despite the reclining guy in front

The problem with private-private mergers is obvious. How do you ascribe relative value to each company? For public companies, there’s a constant voting machine. For private companies, you have an old valuation, cash in bank, burn/revenue, and rosy projections around the future

We had just come off another merger that was almost magical. We bought a company called Lift Media with an identical product, moved all their customers to our platform, only needed one person from their team (not to sound heartless)…so we got all their revenue w/ $0 cost

With SponsorPay, we had more cash and more revenue. We were (internally) bearish on our future growth, since we were late to mobile. They were more bullish on their future growth. We both were probably showing a bit more bravado during the negotiations – my opening slide here

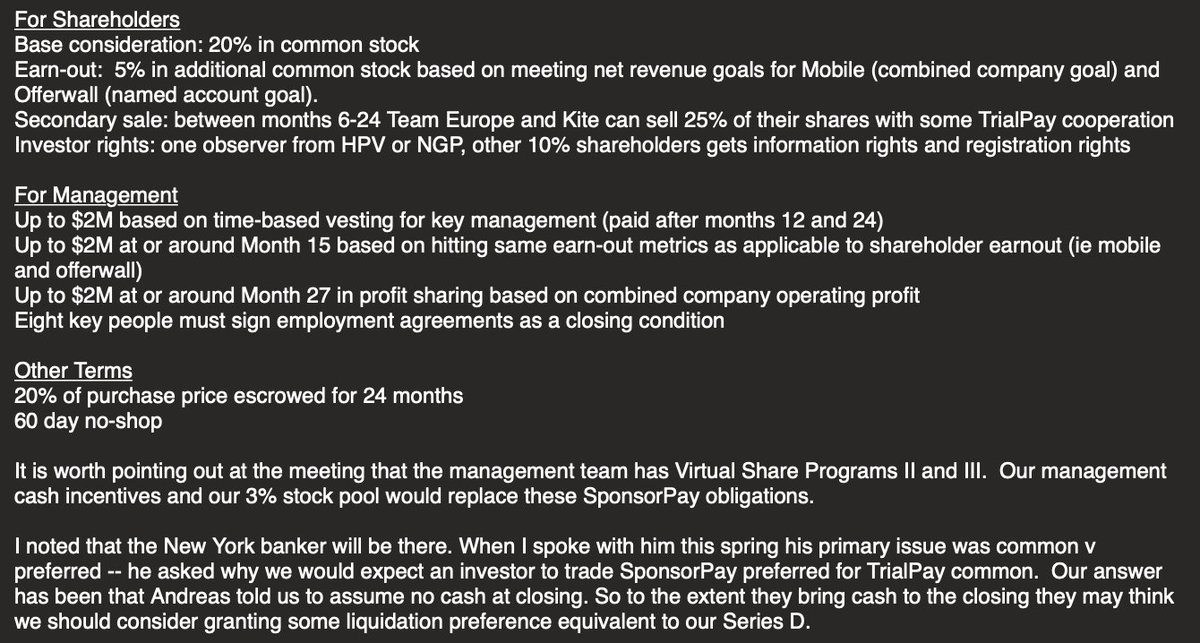

After looking at their financials and our relative cash positions, here’s what we offered (I figure the statute of limitations is up on sharing this stuff since neither company exists anymore! SponsorPay became Fyber became Digital Turbine, so you know how the story ends)

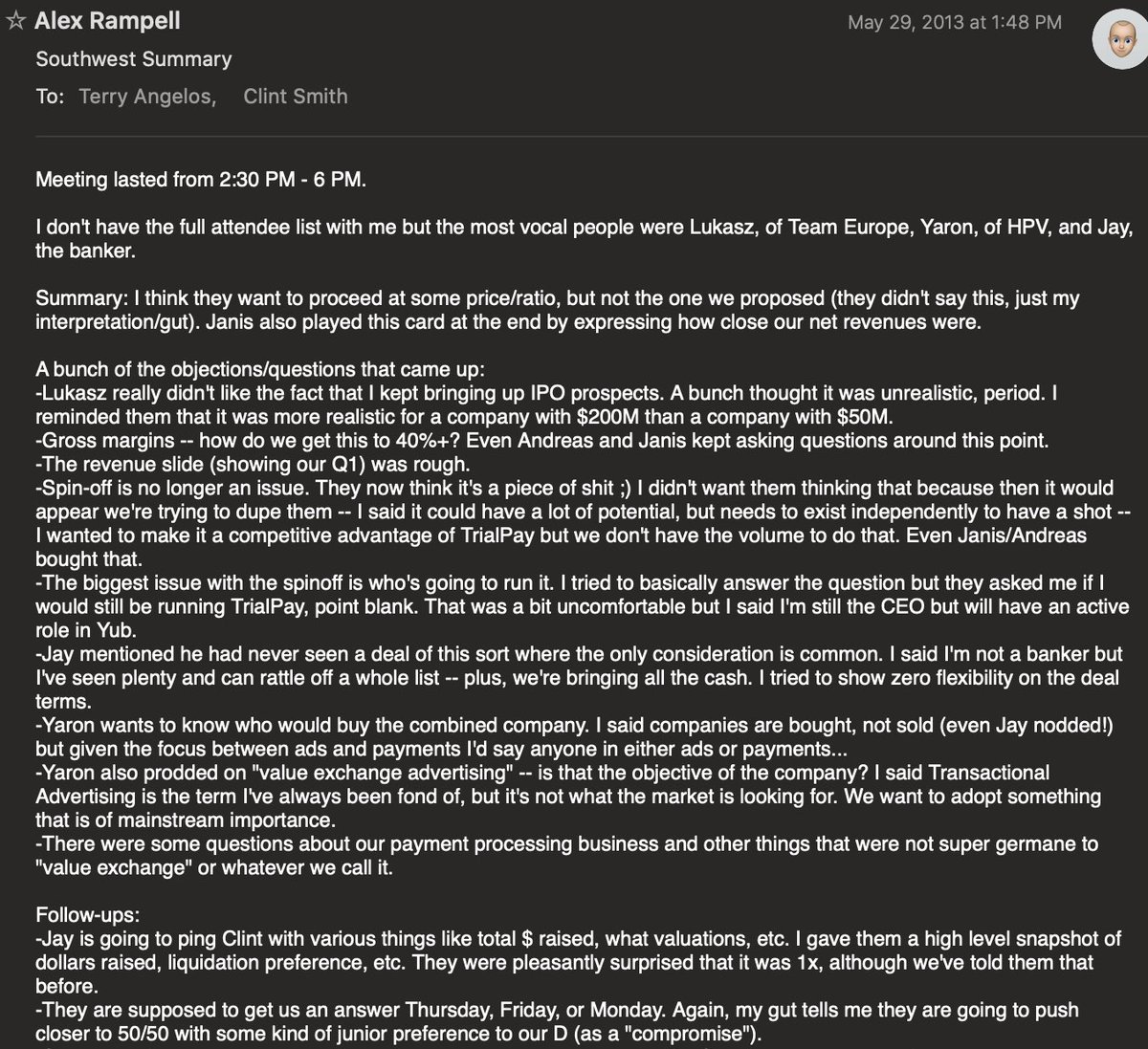

But it was a hard sell. Their investors wanted cash, or at the very least not common stock in our company. We were busy with our spinoff of Yub (see thread in 1). They had hired a banker to try to “shop” our deal. We basically got nowhere, but we didn’t have a sense of urgency

We were also very torn on further diluting our ownership to “double down” on our core strategy by doing a competitive merger. Did it really make sense to give up 20%+ to get more revenue scale but still have 10 other competitors? Like whack-a-mole…with the smallest mole.

I was honest with them that we were busy on our spinoff and likely to see some short term financial pain, and didn’t want to enter the negotiation on “defense” as a result of this. But honestly, my biggest concern was the adage that two turkeys don’t make an eagle

As the year went on, we missed our numbers. They were doing better. We still had more cash. But while we kept opportunistically trying to make this happen, we became further and further apart on price and *strategy*…and after about a year they pulled out, rightfully so.

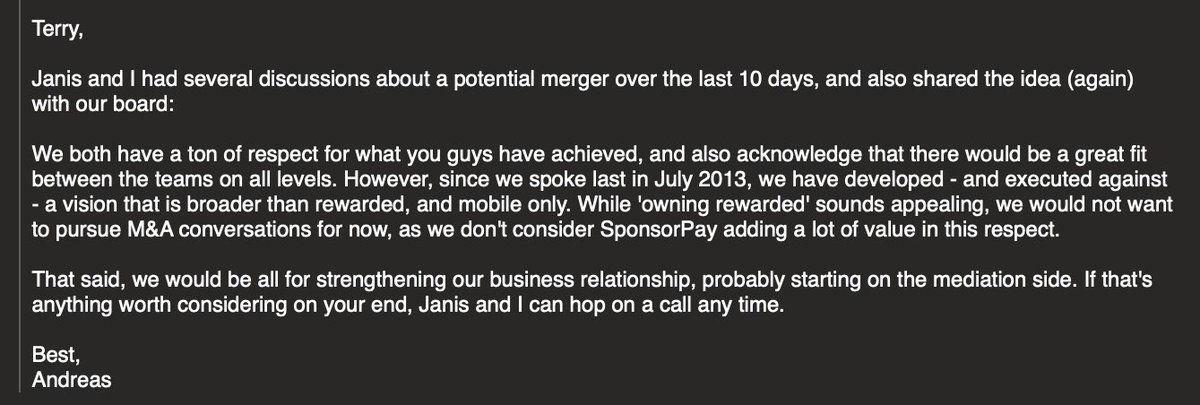

We were pursuing other deals as well. Accel had a challenged company called GetJar which we looked at buying, but we couldn’t get there. I spent a ton of time with PE firms looking at doing a take-private + merger with a public company, Digital River, that needed new tech

This one (DRIV) was arguably the most insane. Merge our unprofitable company plus tech-forward and differentiated team into a profitable but slow-growing public company, steered by a slash-and-burn PE firm. But valuation was even more challenging in this model.

We prostrated ourself in front of every company adjacent to us but our cash position, once our strong point, was weakening. We even had conversations with “that stock might be valuable!” tech companies (future eagles, with us almost acting as VCs) but we had too much rev/opex

In the end, the path we took was the one I wrote about here: https://x.com/arampell/status/1562557849128931328

But several learnings from this experience of private-to-private M&A, including when I’ve seen it work well.

A. 🦃+🦃 ≠ 🦅. Make sure there’s a *real strategy* you can get behind

B. Don’t waste time. If you are cash rich in a bad market, that’s your value. Move fast.

C. “Optics” converge on irrelevance quickly. “Optics” are a reason not to cut burn, not to eliminate products, etc. You’re merging with a private company, not a BigCo

D. Roll-ups are good if they get you to market leadership, but not if they leave you with high fragmentation

E. To quote The Godfather II (and Sun-Tzu): “Keep your friends close, but your enemies closer.” Being on good, text-message-banter terms with the CEOs of all your competitors is *always* a good idea…particular in an environment like this.

Hope this was helpful. I think we’ll see a lot more private-to-private deals, particularly amongst late stage companies, in this market cycle. Fin.