Originally posted as a Twitter thread on May 17, 2023

I’ve often written about how friction/inertia preserves giant gross profit pools in financial services.

The missing link to change this is what I would call a “consumer signup RPA” — which AI can do

RPA: Robotic Process Automation. Take an “API-less” process and “just do it”

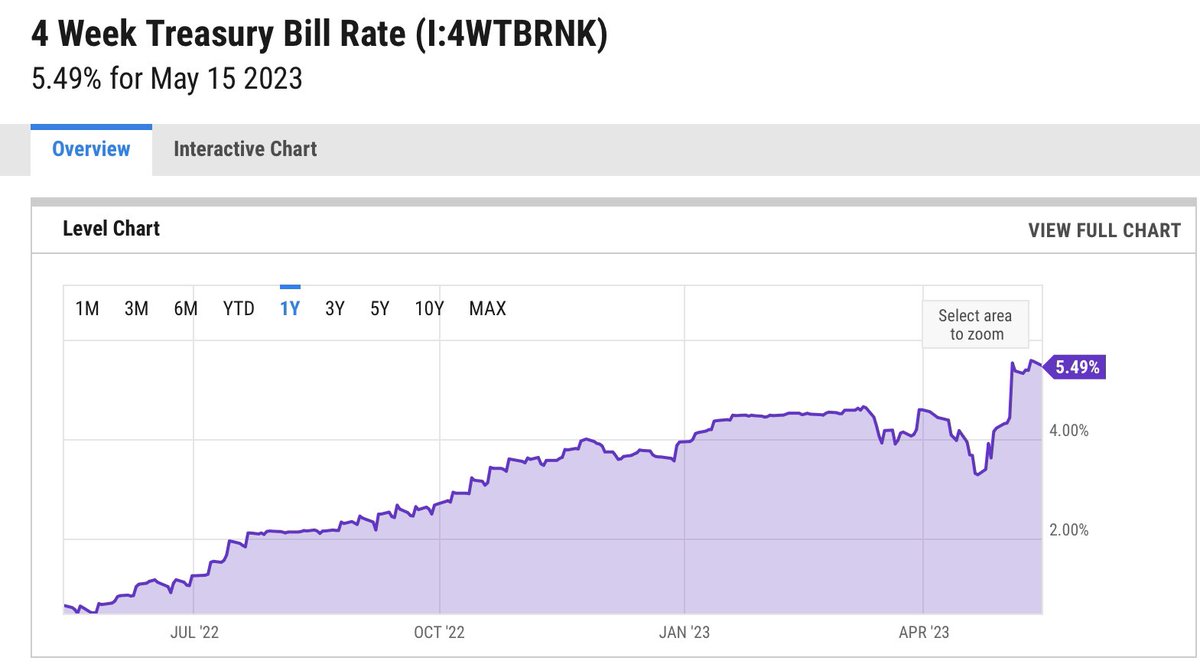

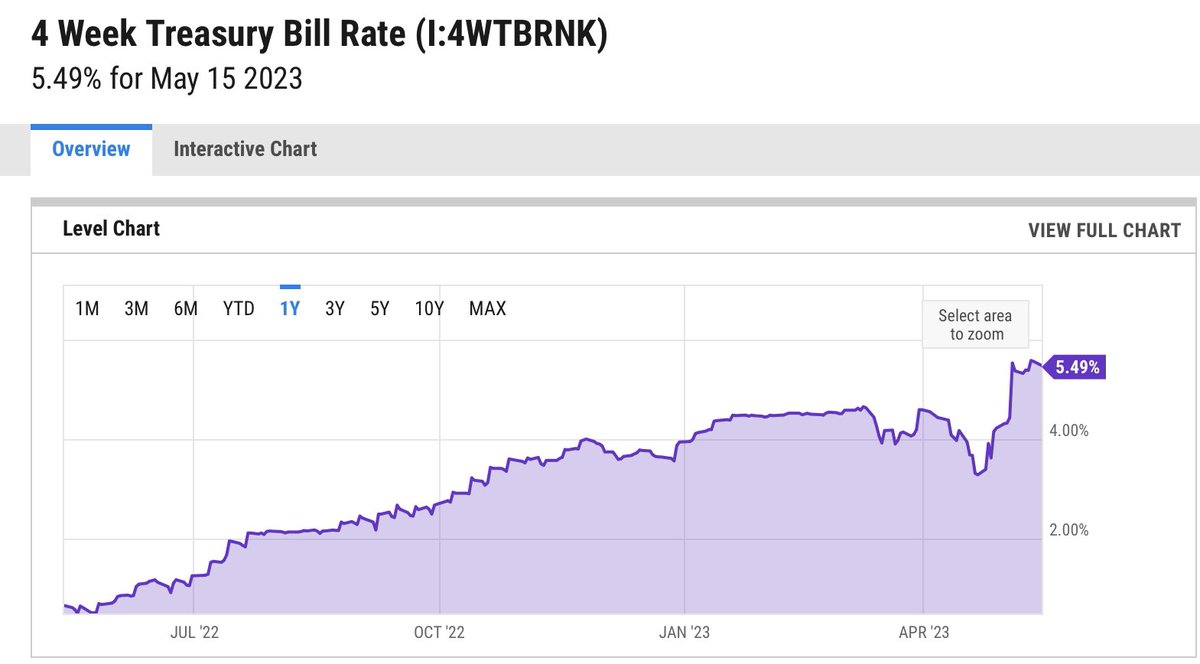

Nowhere is this more true than depository accounts. A 4 week Treasury Bill from the *US Government* pays 5.49% and a 1 year Treasury Bill pays 4.73%.

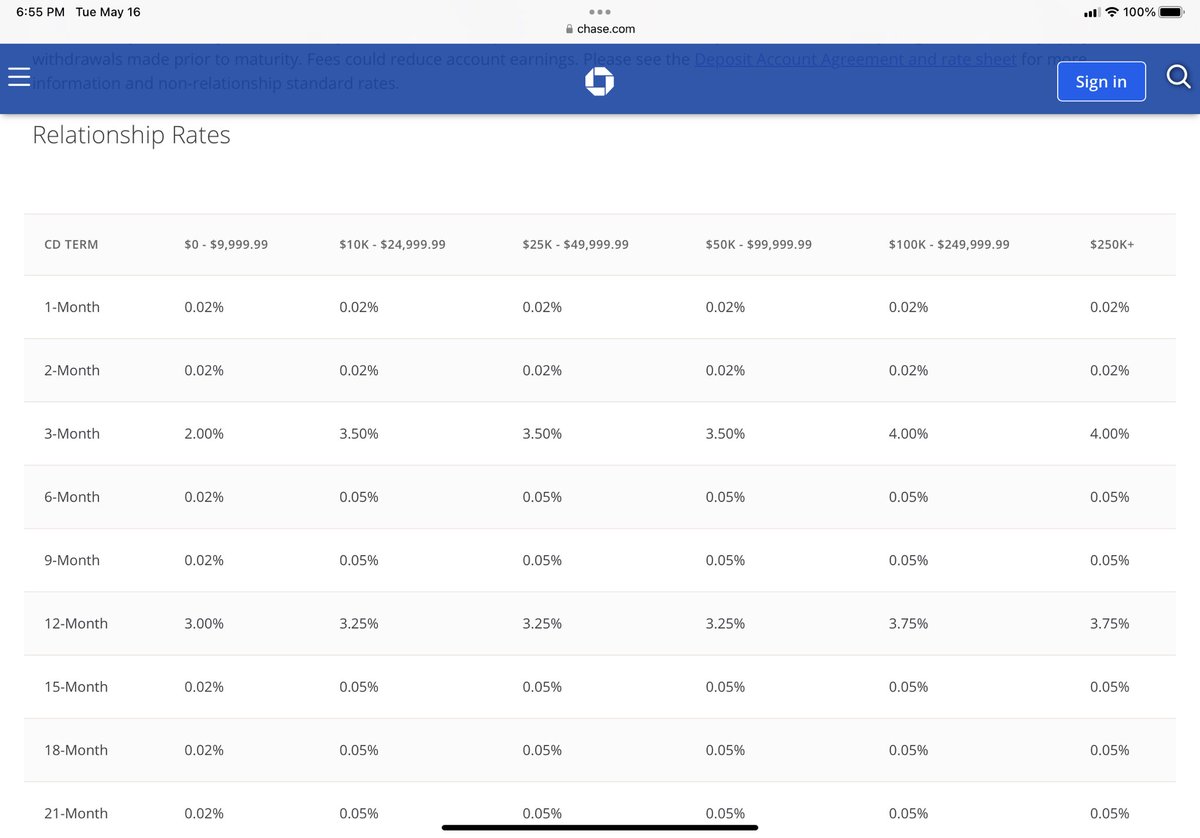

How much does the biggest bank in the US pay for the same…which of course is insured by the same US Government for ONLY up to $250K?

.02% and 3%, respectively…for a higher level of risk. You’d have to be insane to choose a CD with Chase vs a T-bill.

So WHY do consumers leave excess money or buy CDs with Chase? Three reasons:

1. They don’t know what yields are (Chase takes advantage of them)

2. It’s too hard to buy T-bills directly (try signing up for http://treasurydirect.gov)

3. It’s too hard to move money back and forth

The promise of Fintech (and in particular, tools like @Plaid) is that friction/inertia will no longer be an impediment towards consumers switching from the worst services to the best services.

Round One of this was “tools to read” information — let’s import your credit card purchases, or read your checking account number in.

Mobile Wallets have the promise of being a platform for financial services (the App Stores equivalent = financial products). I wrote about this back in 2016:

https://a16z.com/2016/04/25/digital-wallets-fintech-platform/

But AI is also going to transform this, because the incredibly painful (consumer) process of, say, buying short duration T-bills directly from the US government could now be…very easy. Or the seamless movement of money to meet bill pay needs and invest excess cash.

And the missing link for all of this has its technological answer in the form of Generative AI. AI has been used extensively in fintech, but primarily for “scoring” and “approving” things — speeding up backend processes.

But Generative AI is the mirror image: help automatically answer things on behalf of a consumer, bringing a generative robot to a 1990s workflow from a bank (or government) that’s unlikely to embrace, say, RESTful APIs.

And it’s not just about seeking higher yield or lower debt cost, which are particularly salient in today’s higher interest rate environment. Friction/inertia also keep people on their metaphorical financial Flip Phones vs meaningfully better products and experiences

Gen AI also has cost-saving, transformative opportunities for the big guys, too. But if they keep ripping off their customers, they’re finally going to start paying the price as “assistants” make breaking up easy to do…