Originally posted as a Twitter thread on November 18, 2020

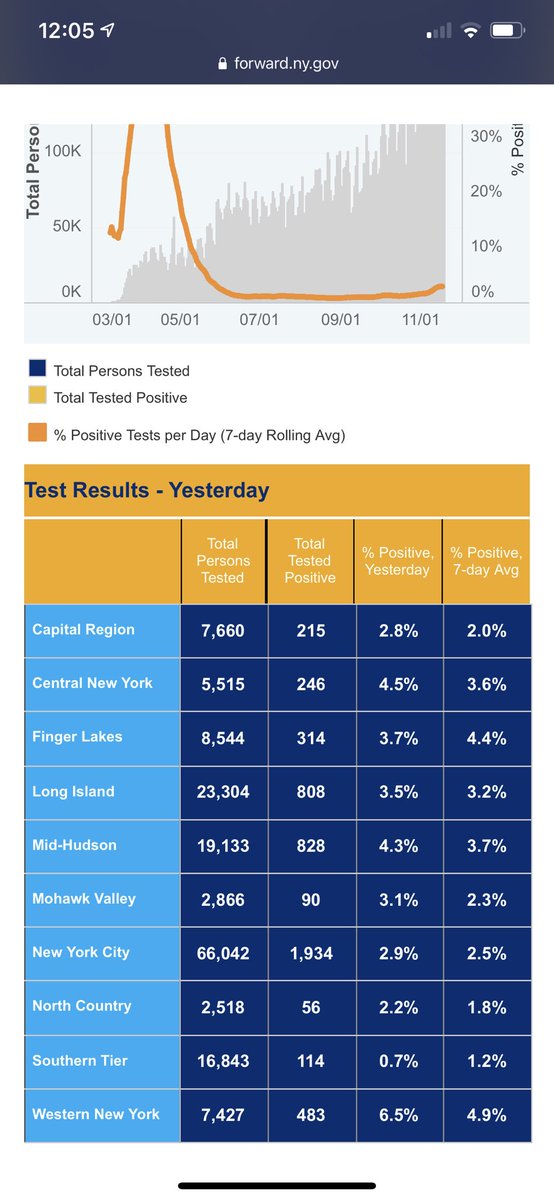

The absurdity of closing ALL SCHOOLS based on the positivity rate of a (presumably selection-biased sick?) less than 1% sample of the population should offend anyone who understands what a fraction is

NYC had 66K tests out of an 8M population. If you only test sick people, you will get a high positivity rate! If you over-test healthy people, you could make Ebola seem pleasant based on its “low positivity rate”

Positivity rate is garbage

Originally posted as a Twitter thread on August 28, 2020

There’s been a lot of misinformation about IPOs — particularly around the narrative of “intentional underpricing” and subsequent IPO pops / “money left on the table.” IPOs aren’t perfect, but the problem isn’t the pop — a sideshow caused by quirky supply/demand imbalances.

The things to fix are aggregating the most demand, blurring the lines between private and public for a seamless transition to being public, and more thoughtful lockup releases, while also ensuring that a company is sufficiently well capitalized.

Many are celebrating SPACs and Direct Listings, which both have their place as valuable tools, as the “death” of the IPO *because* of a misunderstanding of what causes a pop. A price without a quantity is not a price: block sales happen at a discount, M&A at a premium.

But today, an IPO remains the best way to raise a large block of primary capital. It *should* improve, but the way to measure improvement is not pop against low float, but on aggregation of the most demand (*all* investors) in a way that sufficiently capitalizes the company.

There’s a lot more data and examples to back this up in this piece which @skupor and I put together. It’s long but hopefully shows exactly the dynamics and game theory in play around how a company goes public and what’s in a price: https://a16z.com/2020/08/28/in-defense-of-the-ipo/

Originally posted as a Twitter thread on August 16, 2020

Today is August 15, the 49th anniversary of the de facto end of Bretton Woods, creating the fiat currency world we know today. Bitcoin’s birthday is October 31, 2008, but it has a spiritual secondary birthday of today — the widespread beginning of fiat money.

Until August 15, 1971, dollars were backed by gold at a fixed rate of $35/ounce. The dollar was the world’s reserve currency, and underpinning this reserve was this gold backing. Any foreign government could convert their dollars to gold.

At least, they could *conceptually* convert dollars to gold. In reality, by 1971, the US was “writing checks” (printing dollars) that the gold vaults couldn’t “cash” (or metal!) — a run on the gold, so to speak, would metallurgically bankrupt the vaults.

Before 1971, there really wasn’t a notion of purely fiat money with floating exchange rates — or at least not one that was taken seriously. The US was the manufacturing center of the world and dollars were the needed, default currency, backed by gold.

Nixon delivered the following speech on August 15th, announcing this change and codifying it with Executive Order 11615, closing the gold window. It never opened again.

What’s really fascinating is that because gold backed the entire monetary system, owning (non-jewelry) gold was *illegal* from 1933 until 1974. Gold was the settlement ledger for currencies, the true reserve, although the more easily portable/official reserve was the US dollar.

There are many things about a gold standard that make little sense (eg, the supply can increase with a newly discovered mine in South Africa or Russia!) and its inflexibility provides fewer tools for dealing with economic shocks like the Covid one we are dealing with now.

But more so than anything else, gold represented a de facto store of value — and this was *codified* into the financial system until 1971. Seeing as gold now trades at >$2000/ounce, vs $35/ounce in 1971, there’s clearly a divergence between fiat and gold.

And yet gold is: heavy, next to impossible to send around the world (think checks are bad?), hard to divide, and hard to verify. This was NOT a problem before 1971 because the US dollar was none of these things and yet had the backing of/convert ability to gold!

This is why I consider today to be the second birthday of Bitcoin. From 1971-2008, there really wasn’t a financial instrument that had “fixed” dimensions, a reputable store of value but with an easy form of settlement/transmission, which the US dollar until Aug 15 provided.

Given how long it’s been since gold was a reserve currency, and how antiquated gold vaults seem, Bitcoin — for all its flaws — is a logical and superior successor. Particularly given how much money is now being printed by every government, kept in check by…nothing.

There’s an opportunity to turn remote education from a weakness to a strength — from a badly rendered “sage on a stage” (constant in education for 100s of years, but *worse* online!) to individualized instruction. To see why, let’s take a trip to 1984 — not Orwell, but Bloom

Prof Benjamin Bloom wrote a seminal work in 1984 showing that individualized instruction lifted outcomes by 2 standard deviations — outperforming 98% of regular students: http://web.mit.edu/5.95/www/readings/bloom-two-sigma.pdf

But he remarked, it was “too costly for most societies to bear on a large scale”

But the Internet has solved this problem, conceptually! What we need(ed) was a forcing function to abandon the status quo, which Bloom showed is demonstrably worse than individualized tutoring. We potentially have that in Covid, which has incredibly made the status quo *worse*

But Zoom school has none of this. It’s worse in every way than what was already a proven-to-be-suboptimal model for education!

I hope some forward thinking schools will try to go on remote education offense, whereas most are just going on “how do I turn this thing on?” defense.

I encourage everyone to read the Bloom paper. We now have the means (so many great tutoring platforms for a fraction of the cost of private school). We have the motive. And with Covid, we have the opportunity. Fin.

”It’s temporary”: there is NOTHING else to do, people stuck in homes, kids cannot be shipped off to school or daycare, therefore MORE work gets done + people always accessible…but upon opening, people will start playing hooky

“It’s permanent”: the tools for WFH are great (think Slack/Zoom), meeting length gets collapsed to the core substance (1 hr -> 30 mins etc), less travel/commute, accountability via more trackability…

For small companies, “it’s permanent” could have a seismic change on their financials given real estate costs as a % of revenues. But IMHO jury still out on productivity gains/losses given unique nature of this forcible SAH (stay at home!), not just WFH, experiment

And clarifying the first point, parents whose kids are stuck at home cannot go to the beach / play hooky because they need to watch the kids 🙂 Versus normal times when they could.

Originally posted as a Twitter thread on November 06, 2019

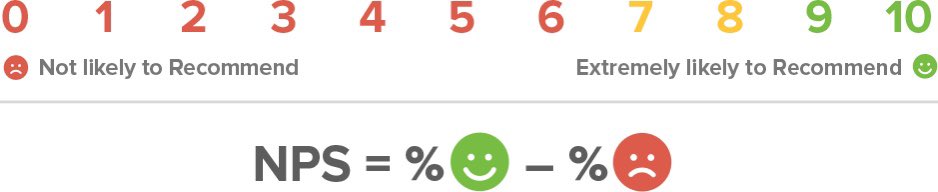

Net Promoter Score (NPS) is, when used properly, a great metric for many businesses. But many startups are trying to tout high scores, not *accurate scores* which is both dangerous and intellectually dishonest.

The classic question is “On a scale of 0 to 10, how likely are you to recommend this company’s product or service to a friend or a colleague?” — so if you have no organic traffic but a high NPS, something doesn’t jive / one of those measurements is wrong

Many companies only (whether by accident or on purpose!) survey their satisfied customers, those who made it through a giant funnel…a form of denominator dishonesty that makes it seem like things are rosy when they are not.

10% NPS might sound terrible, but it could mean you surveyed 10 customers and got nine 8s and one 10. NPS *should* be both a leading and lagging indicator of retention and organic growth, but it loses all meaning when it’s gamed to look rosy. Survey everyone! Face the data!

Originally posted as a Twitter thread on October 27, 2019

This is the top “story” in the NYT app right now. Such a ridiculously sensationalist headline — confusing correlation and causation isn’t enough, might as well figure out how to present a broad policy (Opportunity Zones) through the cartoon-like representation of a “villain”

“Symbol of 80s Excess Stands to Benefit from Flu Shot”

“Man Who Once Met Putin Benefits from Opportunity Zones, Raising Questions of Russian Influence”

“Mnuchin’s High School Girlfriend, Fluent Russian Speaker, Owns Property in Turkey, Raising Questions on Kurdish Policy”

“Grandchildren of Symbol of 1890s Greed, John Rockefeller, Stand to Benefit from Vaccine Developed by Salk”

Originally posted as a Twitter thread on September 18, 2019

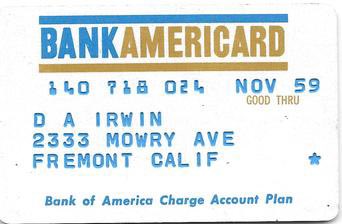

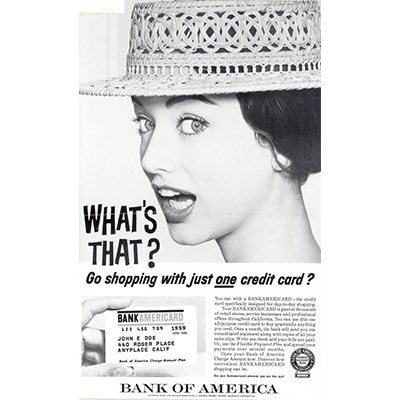

September 18th marks the 61st anniversary of the most valuable network effect of all time: the credit card. How did we get here? Read on. And read @opinion_joe ‘s book “Piece of the Action” for more…

The epicenter of the revolution was Fresno, California. Facebook started with the contained network of Harvard students; the humble credit card started with 60,000 people in Fresno and a prominent company called Bank of America, then a California-only bank.

There was no application. 60,000 people just got a BankAmericard in the mail on September 18, 1958, ready to use.

There were “charge cards” like Diner’s Club before the BankAmericard Fresno drop, but there was no “credit” being extended. And you could go to a bank and get a loan, or get an installment loan for a specific purchase, but in person.

The credit card came out of Bank of America’s corporate think tank, called the “Customer Services Research Department,” run by a 41 year old man named Joe Williams.

Consumers were used to paying on credit, but each line of credit was either specific to a merchant (e.g., Sears), or a burdensome process requiring a new loan (in person) from the bank.

Williams thought the credit card — a multi-merchant product — would fix that. It really had two purposes: convenience and lending.

Fresno at the time had about 250,000 people, and *45% of all Fresno families* were Bank of America customers.

Credit card fees were set at 6% for merchants, and consumers — who just randomly got this card without applying — got between $300 and $500 in instant credit.

The brilliance of the 60,000 person drop is that Williams had effectively started with the chicken, in the classic chicken/egg cold start problem. On day 1, cardholders simply *existed* which permitted BoA to sign up all merchants who didn’t have existing proprietary programs

So Williams started in a seemingly random, highly concentrated town, immediately enlisted existing customers, and focused on fast-moving, small merchants — not the giants like Sears — all backed by a massive advertising campaign.

More than 300 merchants in the city signed up, the first being Florsheim Shoes (still around!).

Within 3 months, BoA was expanding concentrically — to Modesto to the north and Bakersfield to the south, and within a year San Francisco, Sacramento, and Los Angeles. Within 13 months of Fresno, there were 2 million cards issued and 20,000 merchants onboarded.

After the Fresno drop, other banks followed. Chase Manhattan was 5 months later on the east coast.

Williams assumed that collections would be a breeze, that late payments would never cross 4%, and that existing bank credit systems would work. Instead, less than 2 years after Fresno, Joe Williams quit BoA due to a series of disasters. The credit card almost died then+there

Delinquencies were over 20%. Fraud was out of control as criminals figured out how to replicate cards. Merchants (harbinger of things to come) hated paying 6% and the first battles over fees began. Some of them stole from the bank or customers, too.

And more broadly — and this is now illegal — simply giving people cards without having them apply, and without them understanding the consequences of wanton spending, created far more bad debt than BoA had ever seen (on a customer % basis).

The huge losses and mounting pressure almost caused BoA to kill the card program altogether. The founder was ousted. Instead, BoA persevered, and just a few years later BankAmericard turned a profit and grew like a rocketship, transforming how people pay and borrow.

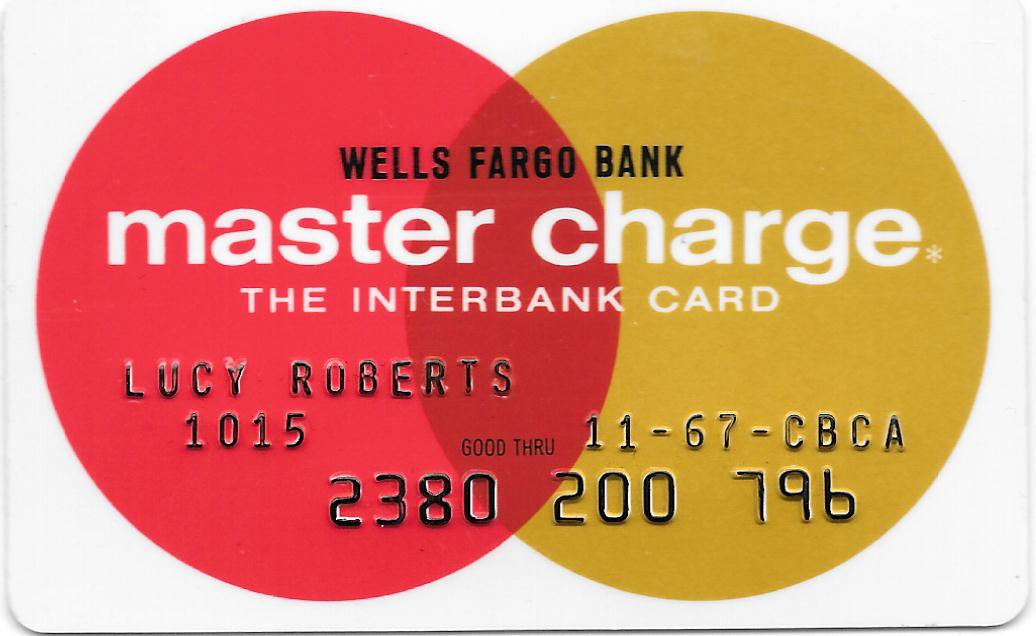

Eventually, BankAmericard became a non-profit consortium called Visa — uniting many banks with competing credit cards. A competing consortium called MasterCharge, later MasterCard, did the same with another set of banks.

Credit cards and payment cards are arguably the most valuable network in the world, with at least $1T of publicly traded market cap (Visa, MasterCard, the banks who issue them, etc)…all starting off in a little town called Fresno, on a random day in September of 1958.

More on how credit cards work today and their history:

Originally posted as a Twitter thread on August 07, 2019

Controlling currency used to mean controlling payments. You print the money as the sovereign; all payments are transacted with that paper. But non-paper payments have changed that and yielded geopolitical risk…

David Ricardo coined the term “comparative advantage” — why trade makes sense. But there’s this issue of geopolitical risk. Growing *zero* food within Country X might be a bad idea if there is a war of anything that interrupts logistics…

So it’s been well-understood, as a matter of national security, that it makes sense to have self-sufficiency in several areas in case trade breaks down

Which brings us back to how currency now has little to do with payments. Governments have very little control over how commerce and payment networks work, or rather, the ability to *keep* them working

The two largest payment networks are in San Francisco (Visa) and Purchase, New York (MasterCard). They are the routers for a huge and growing amount of commerce in *all* countries but they are domiciled in the US, subject to its laws

It’s going to be interesting to see, as paper money goes away and commerce is transacted entirely via payment networks such as these, how governments react. It’s not clear to me that they really understand what’s happening

Now if I’m the UK or France, I might think — hmm, what if that happens to me? In 10 years, things affecting the *commerce* supply, for lack of a better word, will be more influential than anything governments have done in “currency”

China is the only major (non-US) country to have thought this through, as they have their own payment network, China UnionPay, which can interoperate outside of China. But I suspect and expect this to be a bigger deal going forward…

And generally speaking, any network that has an outsize impact on the economy of another country will start being scrutinized more under national security guidelines OR be required to have separate instances that can operate independent of the parent…

For example, imagine that everyone in China took an Uber to work (pre Didi merger). Geopolitical risk having “key economic factor” based in San Francisco — chaos if Uber or the US government cut that off

Food supplies, petroleum, and products of war were the original “national security” risks that couldn’t be subject to plain old free trade. In the 21st century and beyond: NETWORKS.

Fin.

Credit card hack: rather than saving restaurant receipts to make sure I was charged correctly, code the tip. Eg if one’s digit on total is an odd number, cents on the total should be $.57, if even it should be $.42. Leave tip so total adds up to $.42 or $.57 every time.

So when bill comes, if you have a “non-matching” number, you get cheated and can lodge a protest with CC company. And of course the restaurant is supposed to keep your signed receipt as proof, so you don’t have to 🙂

I find that I get cheated every now and then, but don’t want to carry and reconcile receipts at the end of the month nor even think about it. Much easier way!

Clarifying: when your credit card *statement* comes, look for “non-matching” totals (per your own algorithm; mine is not $.42 and $.57, keeping it secret!) and then lodge a complaint if off