Originally posted as a Twitter thread on June 21, 2024

Can’t wait to see the first “incumbent” (in a large software field…like support, CRM, HR, etc) switch from “per-seat” pricing to **per-outcome** pricing.

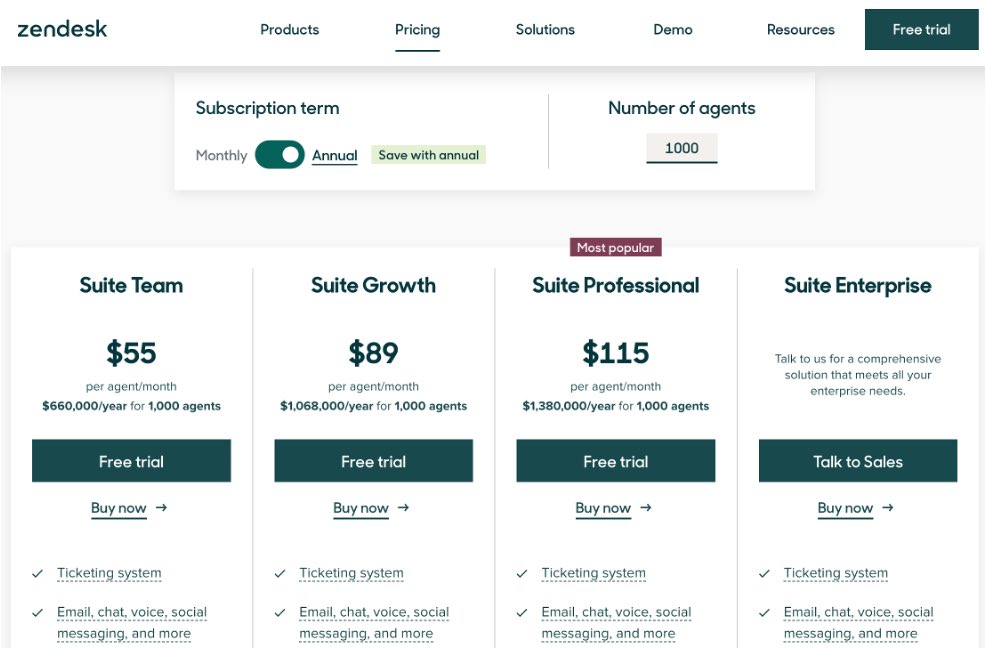

I’m writing an essay on this now, but consider Zendesk at $115/seat per month…or ~$1.4M/year for 1000 agents:

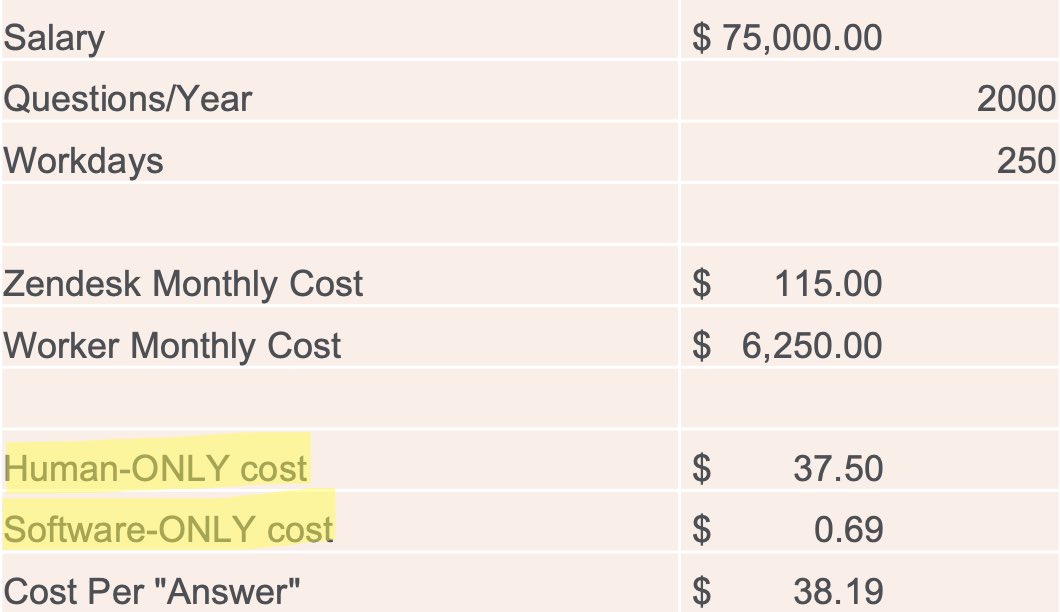

Let’s say an agent is paid all-in $75,000/year and answers 2000 tickets per year.

This makes the human cost of a ticket $37.50, and the software cost $.69.

The human cost obviously massively outstrips the software cost…and unlike software licenses, it can take months to “install” (find, hire, train) a human to occupy that seat. And in many areas there is simply a dearth of qualified humans given licensing latency

In other words, you can’t simply lift wages and produce more workers…if it’s a role that requires licensing or sufficient training (think mortgage brokers, nurses, etc)

Not to mention the fact that it’s hard (and cruel!) to “flex” humans. Southwest Airlines can’t hire tons of humans when bad weather threatens to cancel flights and then fire tons of humans when weather is clear. But software is perfect for this

So: given the rate of improvement in AI for asynchronous support — what will it take for Zendesk to switch from (in the prior example) $115 per seat per month to, say, $10 per successful ticket answered BY Zendesk? Still much cheaper, more flexible, instant provisioning

It’s obviously going to happen, but how should they price this — it’s the ultimate example of value-based pricing? How to have this interact with existing “seats”? How to have teams not feel threatened by their new AI colleagues filling “seats”?

Whole industries will change, and new ones will be created now that software can produce the outcome vs simply be the tool.

Salesforce charges per-seat pricing for salespeople…why not charge per sale?

Maybe Workday can charge for HR “resolutions”

Etc