Originally posted as a Twitter thread on August 15, 2021

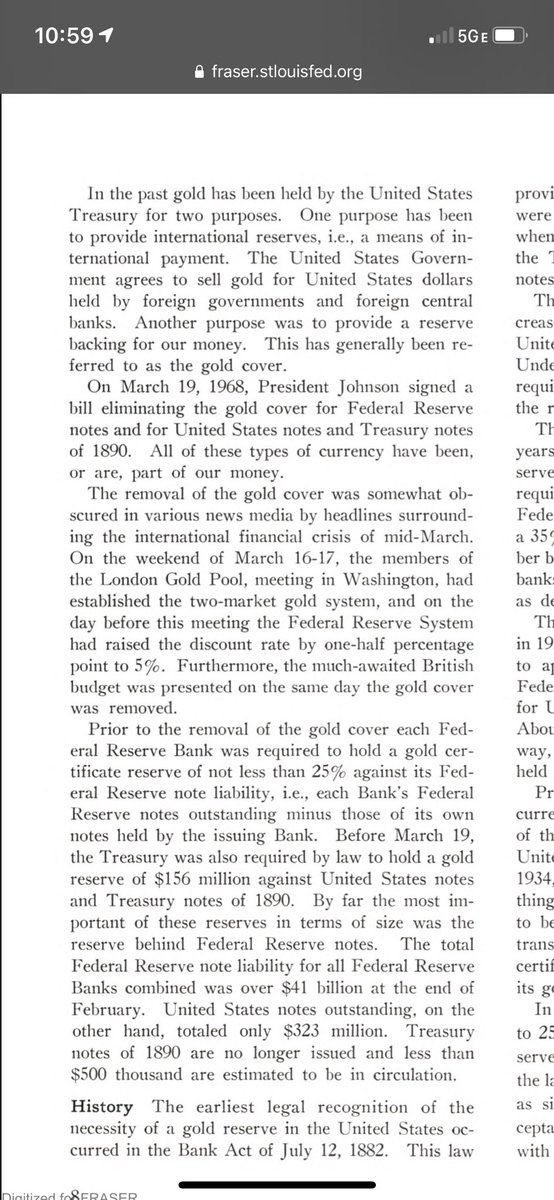

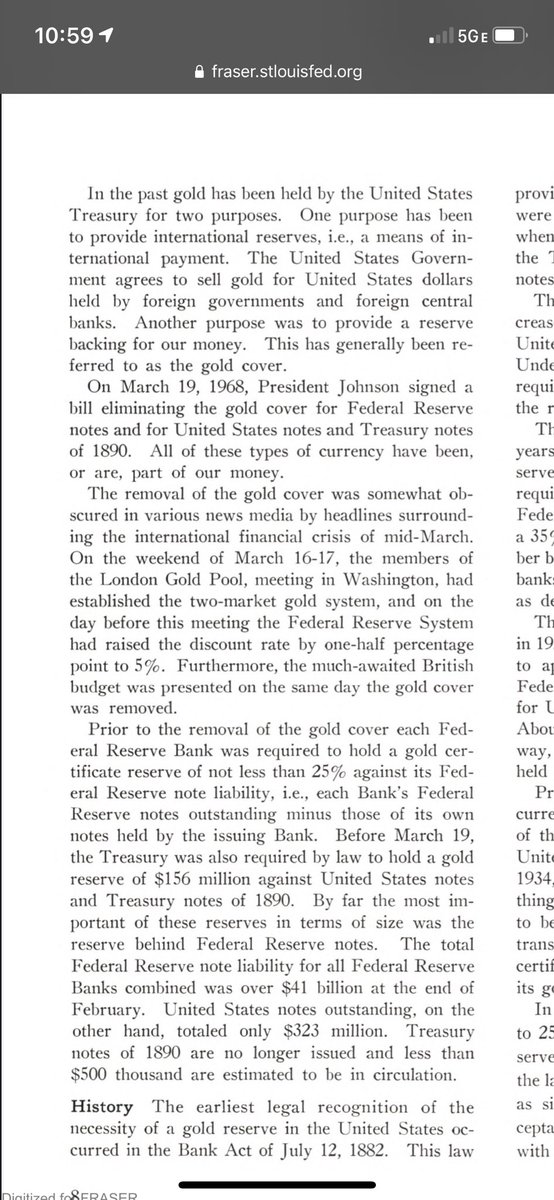

While Bretton Woods and USD gold convertibility formally ended on August 15, 1971, the writing was on the wall for years, particularly once LBJ suspended the 25% Gold Cover for Federal Reserve Notes (and 1890 Treasury Notes) in March 1968:

Originally posted as a Twitter thread on August 16, 2020

Today is August 15, the 49th anniversary of the de facto end of Bretton Woods, creating the fiat currency world we know today. Bitcoin’s birthday is October 31, 2008, but it has a spiritual secondary birthday of today — the widespread beginning of fiat money.

Until August 15, 1971, dollars were backed by gold at a fixed rate of $35/ounce. The dollar was the world’s reserve currency, and underpinning this reserve was this gold backing. Any foreign government could convert their dollars to gold.

At least, they could *conceptually* convert dollars to gold. In reality, by 1971, the US was “writing checks” (printing dollars) that the gold vaults couldn’t “cash” (or metal!) — a run on the gold, so to speak, would metallurgically bankrupt the vaults.

Before 1971, there really wasn’t a notion of purely fiat money with floating exchange rates — or at least not one that was taken seriously. The US was the manufacturing center of the world and dollars were the needed, default currency, backed by gold.

Nixon delivered the following speech on August 15th, announcing this change and codifying it with Executive Order 11615, closing the gold window. It never opened again.

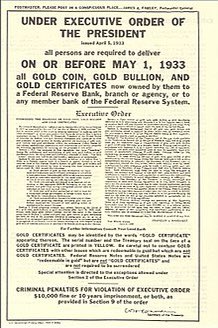

What’s really fascinating is that because gold backed the entire monetary system, owning (non-jewelry) gold was *illegal* from 1933 until 1974. Gold was the settlement ledger for currencies, the true reserve, although the more easily portable/official reserve was the US dollar.

There are many things about a gold standard that make little sense (eg, the supply can increase with a newly discovered mine in South Africa or Russia!) and its inflexibility provides fewer tools for dealing with economic shocks like the Covid one we are dealing with now.

But more so than anything else, gold represented a de facto store of value — and this was *codified* into the financial system until 1971. Seeing as gold now trades at >$2000/ounce, vs $35/ounce in 1971, there’s clearly a divergence between fiat and gold.

And yet gold is: heavy, next to impossible to send around the world (think checks are bad?), hard to divide, and hard to verify. This was NOT a problem before 1971 because the US dollar was none of these things and yet had the backing of/convert ability to gold!

This is why I consider today to be the second birthday of Bitcoin. From 1971-2008, there really wasn’t a financial instrument that had “fixed” dimensions, a reputable store of value but with an easy form of settlement/transmission, which the US dollar until Aug 15 provided.

Given how long it’s been since gold was a reserve currency, and how antiquated gold vaults seem, Bitcoin — for all its flaws — is a logical and superior successor. Particularly given how much money is now being printed by every government, kept in check by…nothing.

Originally posted as a Twitter thread on August 07, 2019

Controlling currency used to mean controlling payments. You print the money as the sovereign; all payments are transacted with that paper. But non-paper payments have changed that and yielded geopolitical risk…

David Ricardo coined the term “comparative advantage” — why trade makes sense. But there’s this issue of geopolitical risk. Growing *zero* food within Country X might be a bad idea if there is a war of anything that interrupts logistics…

So it’s been well-understood, as a matter of national security, that it makes sense to have self-sufficiency in several areas in case trade breaks down

Which brings us back to how currency now has little to do with payments. Governments have very little control over how commerce and payment networks work, or rather, the ability to *keep* them working

The two largest payment networks are in San Francisco (Visa) and Purchase, New York (MasterCard). They are the routers for a huge and growing amount of commerce in *all* countries but they are domiciled in the US, subject to its laws

It’s going to be interesting to see, as paper money goes away and commerce is transacted entirely via payment networks such as these, how governments react. It’s not clear to me that they really understand what’s happening

Now if I’m the UK or France, I might think — hmm, what if that happens to me? In 10 years, things affecting the *commerce* supply, for lack of a better word, will be more influential than anything governments have done in “currency”

China is the only major (non-US) country to have thought this through, as they have their own payment network, China UnionPay, which can interoperate outside of China. But I suspect and expect this to be a bigger deal going forward…

And generally speaking, any network that has an outsize impact on the economy of another country will start being scrutinized more under national security guidelines OR be required to have separate instances that can operate independent of the parent…

For example, imagine that everyone in China took an Uber to work (pre Didi merger). Geopolitical risk having “key economic factor” based in San Francisco — chaos if Uber or the US government cut that off

Food supplies, petroleum, and products of war were the original “national security” risks that couldn’t be subject to plain old free trade. In the 21st century and beyond: NETWORKS.

Fin.

Originally posted as a Twitter thread on September 19, 2018

Visa today has a $328B market cap, bigger than virtually every bank on earth (JPM at $384B is the only one bigger). And yet it started out as a non-profit owned BY banks. How did it become more valuable than its “parents”? https://x.com/VisaNews/status/1042078029114048518

Since Visa intermediates rates between banks (“interchange” between card issuers and merchant acquirers) and clears transactions between issuing banks and acquiring banks, it is the ultimate “central ledger” or platform for finance.

It was originally part of Bank of America, called BankAmericard. But to syndicate this platform beyond BoA, it became a consortium — Visa. Independence (to ensure the central platform didn’t take too much economic rent!) was ensured via non-profit ownership structure

…that is, until 2008 when it went public in the largest US IPO of all time. It reorganized from a non-profit to a for-profit, partially to avoid anti-trust issues (all of the banks get together and decide what to charge merchants…imagine the airlines doing this!)

To me, this is a great example of where/how decentralized networks can preserve true independence (value accrues to network participants vs central player) — and why protocol design, if you will, trumps legal design

Visa is a great and incredibly valuable company. The “protocol” is one of transactional authorization/settlement/clearance. But it was enshrined in a once not-for-profit central actor who today has more value than all but one network participant

Despite a lot of “private blockchain” nonsense out there, this is a great example of how Visa could have or should have been constructed by banks way back when to ensure perpetual independence and inability to capture value as central ledger.

Protocol design matters. And a well thought through protocol is more valuable and protective than lawyers, contracts, and even governments — it will survive all of them.