Originally posted as a Twitter thread on August 15, 2021

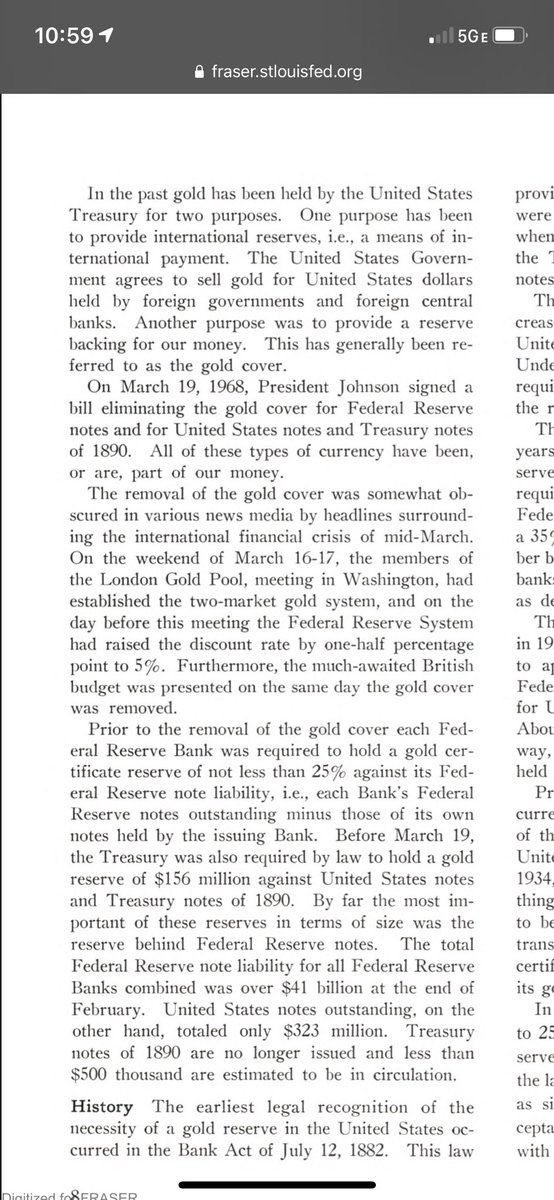

While Bretton Woods and USD gold convertibility formally ended on August 15, 1971, the writing was on the wall for years, particularly once LBJ suspended the 25% Gold Cover for Federal Reserve Notes (and 1890 Treasury Notes) in March 1968:

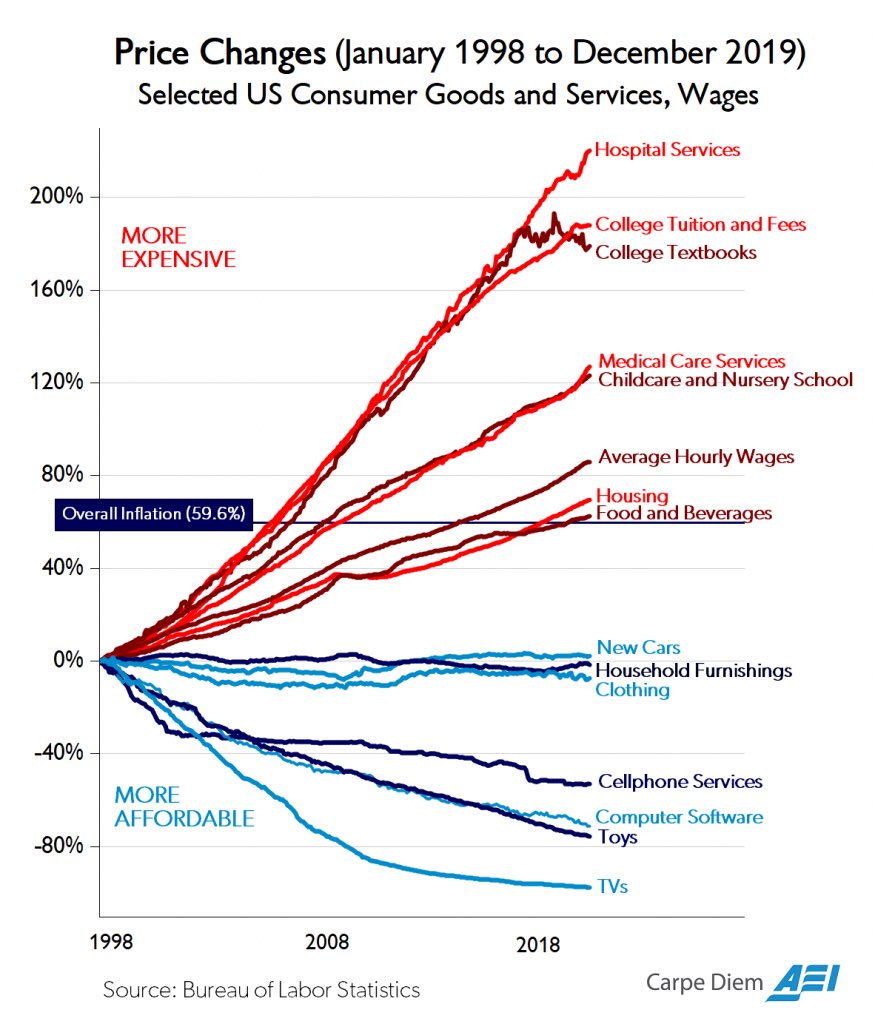

Productivity gains due to technology are the largest source of deflation. $1 buys less today than 1993, but productivity gains offset that for many goods

There’s no doubt that medicine has better outcomes today than, say, 1935. But most other technology-fueled productivity gains make products better AND cheaper…

Originally posted as a Twitter thread on February 11, 2021

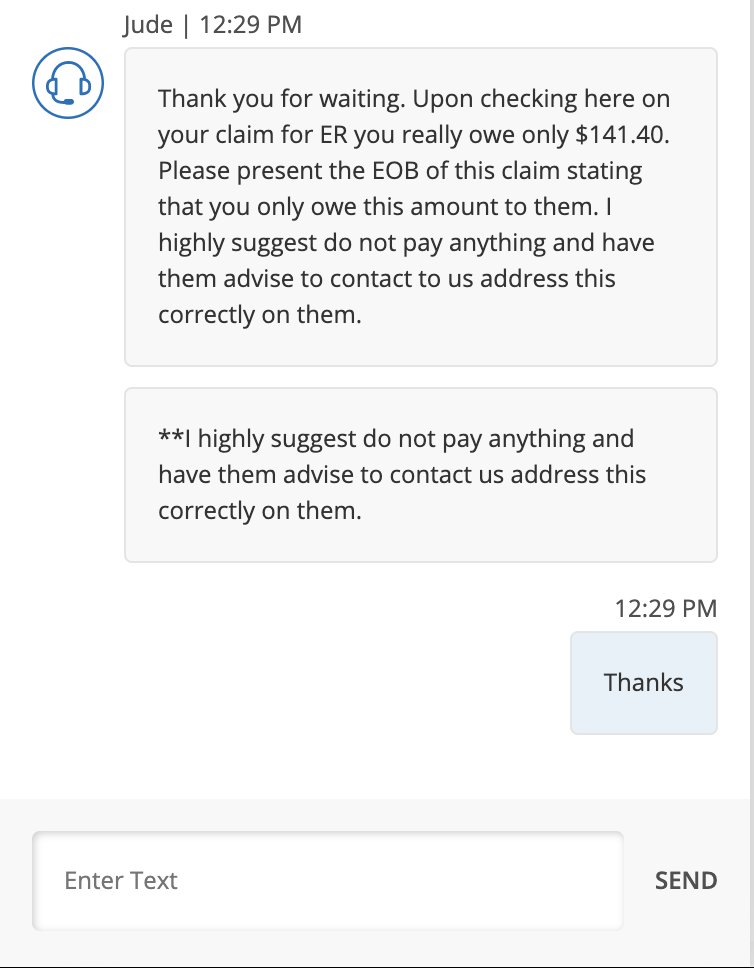

Bureaucracy – in government, the medical system, and more – is a HIGHLY regressive tax in that rich people can pay to solve problems, and the poor must use their time, miss work and lose income…and more.

This is why I love @DoNotPayLaw + @jbrowder1

This is not hyperbole…

I had to go to the ER a few months ago. My bill didn’t match my insurance statement. Insurance company tells me not to pay. Provider threatens to report me to collections. This consumes HOURS of times and damages credit, making borrowing (and living!) more expensive

I am lucky to be able to say “it’s not worth my time” and do just fine — either pay it or deal with the consequences, which are insignificant to me. Millions cannot.

Originally posted as a Twitter thread on January 15, 2021

The Internet has many legacies, but its greatest one is disintermediation — taking out the middleman. And the biggest ever disintermediation — of financial services — is coming to an app near you. This is where government should focus: https://a16z.com/2021/01/15/fintechs-final-frontier/

Governments have monopolies on money and law-enforcement (only the gov’t can legally do those two things, crypto aside!). But there’s almost no way for consumers to interact with central banks! Just like there was no way for consumers to buy airplane tickets w/o travel agents

Want to send a wire? Get access to your PPP loan? Earn interest from the Fed (as banks do via “Interest on Excess Reserves”)? Got to be a bank. Consumers have to go through a travel agent, versus direct. Why can’t your SSN or FEIN be an “account” that can send/receive money?

This is not arguing for “postal banking” or any DMV-style nationalization of banking — which is a terrible idea. But monetary and fiscal policies that require intermediation are simply not as effective as “going direct” — which the internet and fintech allow.

Take interest rates and monetary policy in emerging markets. The Central Bank can/does hike rates to prevent capital flight. Doesn’t really work because banks “intermediate” and don’t provide that rate to consumers…who sell the depreciating currency in favor of USD/EUR.

In many emerging markets, banks hardly make unsecured loans to consumers. They just take deposits and loan to the government. Which is bad for the government, bad for their citizens, bad for their economy, bad for their currency.

More here. Fintech alone can’t solve this — but every single Central Bank should be thinking: how do I go direct? And I would love to see companies and tools (painful as the gov’t “sale” may be) that help facilitate this: https://a16z.com/2021/01/15/fintechs-final-frontier/

Originally posted as a Twitter thread on December 02, 2020

Are high salaries the *cause* or *effect* of expensive housing? In NIMBY-prone areas (hello SF!) where supply is artificially constrained, companies anchored to the geography need to pay a high enough wage to attract talent, which then anchors rent/mortgage payments

Prediction: the current remote-work salary adjustment concept, the Marxian “from each according to his abilities, to each according to his location,” will not last. Why pay people more simply because they choose to live in a more expensive area? Pay them more if they are good!

So looking at lower-cost areas, and paying a discount to prevailing SF wages to get to “parity,” is a crutch of sorts to get to a more sensible end-state: pay a prevailing wage to get the talent. And then let’s see what happens to housing prices…

Home prices will always be based on supply and demand, of course – WFH doesn’t change economics. But “desired location to live” is going to drive that more than “high wage employers” — where those wages could conceptually plummet given increase in supply (global worker pool)

Originally posted as a Twitter thread on August 28, 2020

There’s been a lot of misinformation about IPOs — particularly around the narrative of “intentional underpricing” and subsequent IPO pops / “money left on the table.” IPOs aren’t perfect, but the problem isn’t the pop — a sideshow caused by quirky supply/demand imbalances.

The things to fix are aggregating the most demand, blurring the lines between private and public for a seamless transition to being public, and more thoughtful lockup releases, while also ensuring that a company is sufficiently well capitalized.

Many are celebrating SPACs and Direct Listings, which both have their place as valuable tools, as the “death” of the IPO *because* of a misunderstanding of what causes a pop. A price without a quantity is not a price: block sales happen at a discount, M&A at a premium.

But today, an IPO remains the best way to raise a large block of primary capital. It *should* improve, but the way to measure improvement is not pop against low float, but on aggregation of the most demand (*all* investors) in a way that sufficiently capitalizes the company.

There’s a lot more data and examples to back this up in this piece which @skupor and I put together. It’s long but hopefully shows exactly the dynamics and game theory in play around how a company goes public and what’s in a price: https://a16z.com/2020/08/28/in-defense-of-the-ipo/

Originally posted as a Twitter thread on August 16, 2020

Today is August 15, the 49th anniversary of the de facto end of Bretton Woods, creating the fiat currency world we know today. Bitcoin’s birthday is October 31, 2008, but it has a spiritual secondary birthday of today — the widespread beginning of fiat money.

Until August 15, 1971, dollars were backed by gold at a fixed rate of $35/ounce. The dollar was the world’s reserve currency, and underpinning this reserve was this gold backing. Any foreign government could convert their dollars to gold.

At least, they could *conceptually* convert dollars to gold. In reality, by 1971, the US was “writing checks” (printing dollars) that the gold vaults couldn’t “cash” (or metal!) — a run on the gold, so to speak, would metallurgically bankrupt the vaults.

Before 1971, there really wasn’t a notion of purely fiat money with floating exchange rates — or at least not one that was taken seriously. The US was the manufacturing center of the world and dollars were the needed, default currency, backed by gold.

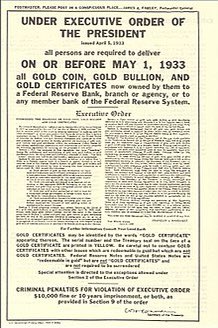

Nixon delivered the following speech on August 15th, announcing this change and codifying it with Executive Order 11615, closing the gold window. It never opened again.

What’s really fascinating is that because gold backed the entire monetary system, owning (non-jewelry) gold was *illegal* from 1933 until 1974. Gold was the settlement ledger for currencies, the true reserve, although the more easily portable/official reserve was the US dollar.

There are many things about a gold standard that make little sense (eg, the supply can increase with a newly discovered mine in South Africa or Russia!) and its inflexibility provides fewer tools for dealing with economic shocks like the Covid one we are dealing with now.

But more so than anything else, gold represented a de facto store of value — and this was *codified* into the financial system until 1971. Seeing as gold now trades at >$2000/ounce, vs $35/ounce in 1971, there’s clearly a divergence between fiat and gold.

And yet gold is: heavy, next to impossible to send around the world (think checks are bad?), hard to divide, and hard to verify. This was NOT a problem before 1971 because the US dollar was none of these things and yet had the backing of/convert ability to gold!

This is why I consider today to be the second birthday of Bitcoin. From 1971-2008, there really wasn’t a financial instrument that had “fixed” dimensions, a reputable store of value but with an easy form of settlement/transmission, which the US dollar until Aug 15 provided.

Given how long it’s been since gold was a reserve currency, and how antiquated gold vaults seem, Bitcoin — for all its flaws — is a logical and superior successor. Particularly given how much money is now being printed by every government, kept in check by…nothing.

Originally posted as a Twitter thread on September 18, 2019

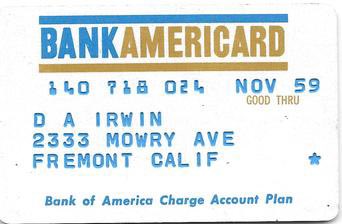

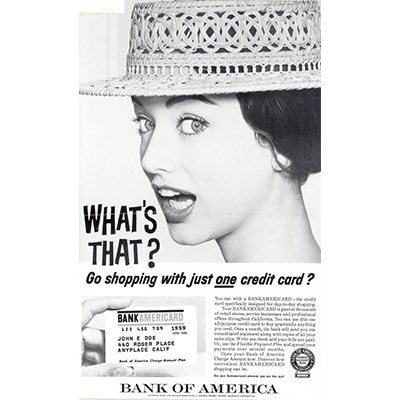

September 18th marks the 61st anniversary of the most valuable network effect of all time: the credit card. How did we get here? Read on. And read @opinion_joe ‘s book “Piece of the Action” for more…

The epicenter of the revolution was Fresno, California. Facebook started with the contained network of Harvard students; the humble credit card started with 60,000 people in Fresno and a prominent company called Bank of America, then a California-only bank.

There was no application. 60,000 people just got a BankAmericard in the mail on September 18, 1958, ready to use.

There were “charge cards” like Diner’s Club before the BankAmericard Fresno drop, but there was no “credit” being extended. And you could go to a bank and get a loan, or get an installment loan for a specific purchase, but in person.

The credit card came out of Bank of America’s corporate think tank, called the “Customer Services Research Department,” run by a 41 year old man named Joe Williams.

Consumers were used to paying on credit, but each line of credit was either specific to a merchant (e.g., Sears), or a burdensome process requiring a new loan (in person) from the bank.

Williams thought the credit card — a multi-merchant product — would fix that. It really had two purposes: convenience and lending.

Fresno at the time had about 250,000 people, and *45% of all Fresno families* were Bank of America customers.

Credit card fees were set at 6% for merchants, and consumers — who just randomly got this card without applying — got between $300 and $500 in instant credit.

The brilliance of the 60,000 person drop is that Williams had effectively started with the chicken, in the classic chicken/egg cold start problem. On day 1, cardholders simply *existed* which permitted BoA to sign up all merchants who didn’t have existing proprietary programs

So Williams started in a seemingly random, highly concentrated town, immediately enlisted existing customers, and focused on fast-moving, small merchants — not the giants like Sears — all backed by a massive advertising campaign.

More than 300 merchants in the city signed up, the first being Florsheim Shoes (still around!).

Within 3 months, BoA was expanding concentrically — to Modesto to the north and Bakersfield to the south, and within a year San Francisco, Sacramento, and Los Angeles. Within 13 months of Fresno, there were 2 million cards issued and 20,000 merchants onboarded.

After the Fresno drop, other banks followed. Chase Manhattan was 5 months later on the east coast.

Williams assumed that collections would be a breeze, that late payments would never cross 4%, and that existing bank credit systems would work. Instead, less than 2 years after Fresno, Joe Williams quit BoA due to a series of disasters. The credit card almost died then+there

Delinquencies were over 20%. Fraud was out of control as criminals figured out how to replicate cards. Merchants (harbinger of things to come) hated paying 6% and the first battles over fees began. Some of them stole from the bank or customers, too.

And more broadly — and this is now illegal — simply giving people cards without having them apply, and without them understanding the consequences of wanton spending, created far more bad debt than BoA had ever seen (on a customer % basis).

The huge losses and mounting pressure almost caused BoA to kill the card program altogether. The founder was ousted. Instead, BoA persevered, and just a few years later BankAmericard turned a profit and grew like a rocketship, transforming how people pay and borrow.

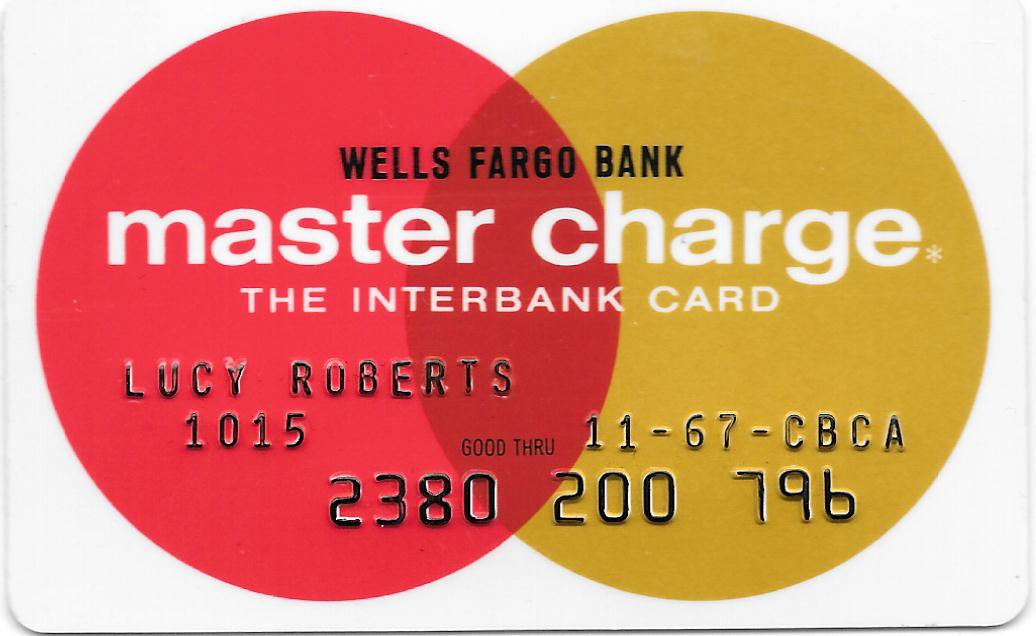

Eventually, BankAmericard became a non-profit consortium called Visa — uniting many banks with competing credit cards. A competing consortium called MasterCharge, later MasterCard, did the same with another set of banks.

Credit cards and payment cards are arguably the most valuable network in the world, with at least $1T of publicly traded market cap (Visa, MasterCard, the banks who issue them, etc)…all starting off in a little town called Fresno, on a random day in September of 1958.

More on how credit cards work today and their history:

So why don’t consumers do this? It’s WAAAY too complicated for, in this case, an average of $271 per month. Add in the paradox of choice (refinance with whom?), getting stuff notarized, getting both spouses to sign, and hidden fees…and it’s easier to do nothing

Roboadvisors have been around for a while focused on investing assets and optimizing portfolios, but I believe the bigger opportunity is on roboadvising debt — and this has potentially the gravest impact to banks who *make money on friction* (which is all banks!)

There are lots of refinance companies out there, but the biggest opportunity is to do it all automagically for consumers whenever savings can be had (including shifting unsecured debt into secured debt). Refinance as a service, not leadgen to open yet another account

Banks are effectively the biggest “managed marketplaces” out there, between depositors and borrowers. Both sides are getting screwed over by a giant take rate protected by friction (too hard to switch) — with banks earning healthy spreads and record profits

Originally posted as a Twitter thread on September 19, 2018

Visa today has a $328B market cap, bigger than virtually every bank on earth (JPM at $384B is the only one bigger). And yet it started out as a non-profit owned BY banks. How did it become more valuable than its “parents”? https://x.com/VisaNews/status/1042078029114048518

Since Visa intermediates rates between banks (“interchange” between card issuers and merchant acquirers) and clears transactions between issuing banks and acquiring banks, it is the ultimate “central ledger” or platform for finance.

It was originally part of Bank of America, called BankAmericard. But to syndicate this platform beyond BoA, it became a consortium — Visa. Independence (to ensure the central platform didn’t take too much economic rent!) was ensured via non-profit ownership structure

…that is, until 2008 when it went public in the largest US IPO of all time. It reorganized from a non-profit to a for-profit, partially to avoid anti-trust issues (all of the banks get together and decide what to charge merchants…imagine the airlines doing this!)

To me, this is a great example of where/how decentralized networks can preserve true independence (value accrues to network participants vs central player) — and why protocol design, if you will, trumps legal design

Visa is a great and incredibly valuable company. The “protocol” is one of transactional authorization/settlement/clearance. But it was enshrined in a once not-for-profit central actor who today has more value than all but one network participant

Despite a lot of “private blockchain” nonsense out there, this is a great example of how Visa could have or should have been constructed by banks way back when to ensure perpetual independence and inability to capture value as central ledger.

Protocol design matters. And a well thought through protocol is more valuable and protective than lawyers, contracts, and even governments — it will survive all of them.