Can’t wait to see the first “incumbent” (in a large software field…like support, CRM, HR, etc) switch from “per-seat” pricing to **per-outcome** pricing.

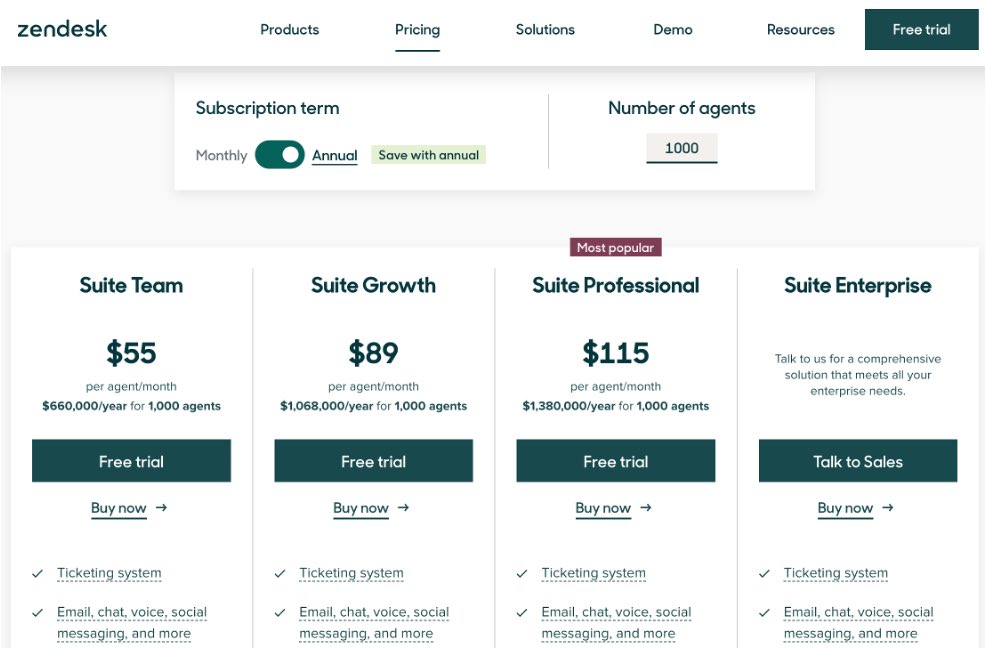

I’m writing an essay on this now, but consider Zendesk at $115/seat per month…or ~$1.4M/year for 1000 agents:

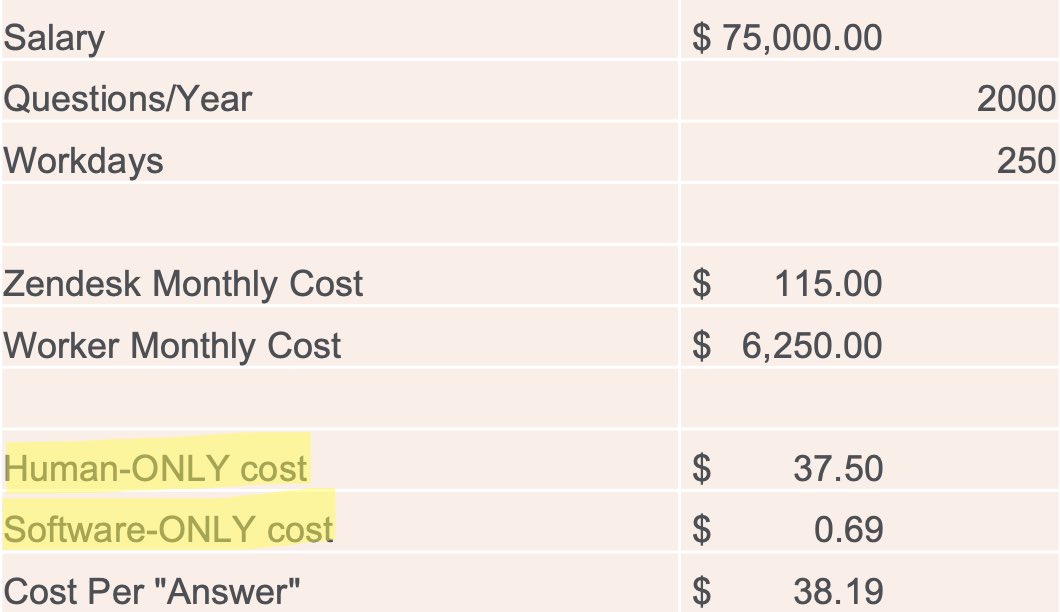

Let’s say an agent is paid all-in $75,000/year and answers 2000 tickets per year.

This makes the human cost of a ticket $37.50, and the software cost $.69.

The human cost obviously massively outstrips the software cost…and unlike software licenses, it can take months to “install” (find, hire, train) a human to occupy that seat. And in many areas there is simply a dearth of qualified humans given licensing latency

In other words, you can’t simply lift wages and produce more workers…if it’s a role that requires licensing or sufficient training (think mortgage brokers, nurses, etc)

Not to mention the fact that it’s hard (and cruel!) to “flex” humans. Southwest Airlines can’t hire tons of humans when bad weather threatens to cancel flights and then fire tons of humans when weather is clear. But software is perfect for this

So: given the rate of improvement in AI for asynchronous support — what will it take for Zendesk to switch from (in the prior example) $115 per seat per month to, say, $10 per successful ticket answered BY Zendesk? Still much cheaper, more flexible, instant provisioning

It’s obviously going to happen, but how should they price this — it’s the ultimate example of value-based pricing? How to have this interact with existing “seats”? How to have teams not feel threatened by their new AI colleagues filling “seats”?

Whole industries will change, and new ones will be created now that software can produce the outcome vs simply be the tool.

Salesforce charges per-seat pricing for salespeople…why not charge per sale?

Maybe Workday can charge for HR “resolutions”

Etc

Before you launch a new product, one of the most counterintuitively important things to do is to plan for how to kill or exit the product. FAST.

This isn’t as simple as it sounds…and it’s crucial for companies with multiple products or consulting work.

My company, TrialPay, was the leading company doing “offers” en lieu of payment. I realized we strategically needed to be in the more commodity payment processing space, more background here: http://www.arampell.org/2015/11/04/distribution-v-innovation/

We built this payment business to 9 figures of payment volume, but didn’t have sufficient focus to make it our top priority, and we were nowhere close to being #1 in the space. (Most value accrues to the #1 or MAYBE top 2-3 players). But our core clients were using it!

This is why a pre-mortem is so important. We used our goodwill and “bundle economics” to cross-sell current customers on what had become a 2nd rate product. If we shut it down, they’d be PISSED and would potentially dump us for our core product!

So what to do? We were honestly stuck. Against the backdrop of massive pressure against our core business, per thread below. We needed to focus on what we were great at. https://x.com/arampell/status/1562557849128931328?s=20

Our only answer was to find a home / new product for our customers. I called the then CEO of Braintree and basically offered our customers and product for free — he said “what’s the catch?” It’s not every day that a competitor (us) voluntarily capitulates…

But our real competition was FOCUS. It was clear we had lost the battle to be #1 in raw payment processing. Dedicating resources to be a distant #8 was more expensive than getting nothing for this asset.

The next step was to gingerly mention this to our clients without having them ditch us for our core, profitable offers product. This was hard. But we made it work.

Being an entrepreneur means being able to make the best of the hand you are dealt but also knowing when and how to switch tables. And switching tables dispassionately — when you have teams and customers “stuck” to the old table — is hard

This is one of the reasons to be VERY cautious about doing consulting work. Building a custom product for a marquee client sounds great to make ends meet, but you can’t kill it! You’ve just added a liability to your balance sheet. You have to support it…forever!

Theoretically you could kill it, but then good luck selling another product to that company. If you need to do a RIF, and you’ve gotten pre-paid for this software, how do you cut the team supporting this product that represents 0% of your future…?

So always, always think about this hidden “liability” on your business. Before you customize, contract, or test something…have a well thought through plan to KILL your new thing. Bake it into all your processes, contracts, code, culture, etc.

When starting a company, can you get to *5 customers*? Who are they? Why will they trust YOU?

As a VC, these are questions I always try to ask (selling B2B). I’ll tell my story of how my company got our first 5, and why 5 seems like a good heuristic of “you’ve got something”

I love the term “productize” — it effectively means turn a “service” or “consulting” project into a repeatable widget. Does a large n of customers need/want the same thing, or *roughly* the same thing with few customizations? Then…it *might* just be productizable

If you get your Uncle or Cousin to use your product, maybe it was a favor…which is a feature (not bug) if it indeed is the SAME product you can sell to a few other strangers. But a lot of times a “few” customers is just a collection of favors and is Fool’s Gold…

Fool’s Gold because it’s just not repeatable and hides brutal market feedback. You can only have so many college roommates, cousins, and uncles. But if you get 5 distinct customers to “agree” on the same set of features, it’s a very good sign and you’re off to the races.

TrialPay started off as something I used for my own freemium software business. “Don’t want to pay $10 for my app? Get it for free if you sign up for Netflix or get a Discover Card or shop at Gap.” It worked great so I decided to turn it into a company…and raise venture $

But a lot of times ideas/companies come in waves — two other companies basically popped up at the same exact time. Identical idea/value prop. Lift Media (@jmurz) and MyOfferPal (later merged/renamed TapJoy). We all pitched the same VCs within weeks in 2006!

I had a key advantage over them in that I still had my software business so could “create” traction — I was my own first customer. Could figure out if things were working. But more importantly, it gave me credibility in “my community” of freemium software developers.

After starting the company, my co-founder @terryangelos and I went to the “Shareware Industry Conference” in Denver…and we signed several customers there, the largest being WinZip. I gave a talk on my results with my own products…so had the credibility and knew this niche

This was so niche that few outside of the industry even knew of this conference…or had the credibility/connections with this somewhat esoteric group of businesses/people. I remember meeting @bradfurber and @allennieman there…at a relatively unknown (but big revs!) company…

But sometimes, particularly when building a “transactional” business (versus “per-seat” where you know # of employees), there are these “diamond in the rough” customers that turn out to be huge. Brad and Allen’s company (Sammsoft) was one of them. Huge client.

My *now* friend @jmurz of Lift Media was super smart, incredibly hard-working, and was building his nearly-identical business…he was my arch-nemesis at the time!!…but we got a big early lead, which later turned into a big fundraising advantage too…

And honestly it was almost entirely because:

A. I had a captive early customer that would do anything I wanted (customer was…me!)

B. I found a bunch of other customers that “looked” like me — no chasm to cross. “I sell $30 Windows software, you sell $30 Windows software”

As we expanded, this was one thing that never ceased to amaze. Companies *across* verticals often have a hard time being the first in their space…getting Skype or Fandango to use us was not really helped by the fact we had WinZip. “Oh, that’s totally different.”

My advice to developing a killer product and go-to-market — and ensuring you don’t end up over-engineering into a void or losing to another competitor — is that you need both a founding team (founders/employees) and a founding *group of customers*

You need some vision, flexibility, and fortitude to make sure YOU are building the product, not your customers — otherwise it’s the Henry Ford “if I asked my customers what they wanted, they would have said a faster horse”

But you also need real market feedback so getting some friendly customers — who are willing to bet on you (kind of crazy to run your business on a money-losing startup!!), ride out some bumps, and give more than an occasional testimonial…is crucial

So sometimes 0->1 is not all that hard (if “1” is your Uncle). Getting 1->5 is actually what’s hard…synthesizing feedback, and building that trust that no 12-months-of-cash-left startup is just “entitled” to. It’s a crucial ingredient to success.

Some ideas on how to do this:

A. Give equity to your early customers or have them invest

B. Have no shame plumbing every connection you can – favors and believers

C. I tend to think the best companies are ones that came out of personal experience / you can be 1st customer

Thanks to @1nternetjack for the idea on this one. And watch this scene from one of the best Simpsons episodes ever, about the perils of *overly* conforming your product to just one customer:

Companies are (almost always) bought, not sold. This means somebody needs to *want to buy* your company. Ideally this happens organically. But how do you, as a founder/CEO, expedite this…particularly when you KNOW you’re hitting a wall?

“Planting an idea”

Inception is one of the greatest movies of all time (watch the clip). The whole premise is about implanting an idea in somebody’s mind…the inception of an idea. “If you’re going to perform inception, you need imagination”

There are probably three types of acquisitions: A. Acquihire (want team, not business or product) B. Product/“Trade Sale” (want product or to repurpose product, acquirer has distribution) C. Business “left-alone” (give existing business more resources to grow faster)

Especially for Acquihires and Product-oriented sales, you need to get to know your prospective “buyers” *far in advance* of “needing” or wanting to sell your company. Two independent variables exist: when they can/want to buy, and when you want to sell…rarely do they align!

Buyers aren’t companies, they’re *people at companies*, and generally people with P&L responsibility. Often somebody climbing the corporate ladder who wants to make a big splash and is anxious to ship something taking way too long internally. Or a new VP who needs a team ASAP.

Almost every large company has a corporate development person/team. Their job is to close deals, not to ideate – once you are “bought” you’re not working for the VP of Corp Dev. You’re working for whatever division and whatever person wanted your product. Focus on GMs/PMs/VPs.

Focusing on product/trade-sales: the key thing is to figure out where 1+1=3, or how your product might fit within the org. At TrialPay we showed ads around transactions — what if PayPal could stick our ads in every purchase receipt? Would generate >$1B…that was our pitch.

The goal is not to approach the company (or person) with “please buy me” — it’s not like a fundraise. That’s massively counterproductive. It’s to propose a BD deal that is just standard operating procedure for your independent company. Which hopefully happens regardless!

You CANNOT PUSH A STRING. This was a lesson I learned very painfully. Do not be aggressive; this isn’t like closing an oversubscribed funding round. Articulate a vision for how your product fits and is a win-win for both, try to get a test/integration/contract in place.

The true “inception” for the more valuable product-oriented acquisitions is “wow, we shouldn’t let this be a BD-deal…we NEED to own this.” *That* is when you can (possibly) sell your company for a lot of money.

Even so — most companies have a culture of “anyone can say no, nobody can say yes” — you need to sell horizontally, deal with people who are threatened (“we can build it ourselves!”), and recognize you’ll be judged “on the present”.

“Being Judged on the Present” is a very big deal (see blog post) — you need to steer things to what your product, or a variant of it, WILL look like. Make a real polished demo. Put real work into it. Your “existing” product or team or tech might be used against you.

This is why “imagination” is so key — your product currently does X, but there are probably 5 giant companies where a few tweaks/changes to it – X’ – could accomplish a major objective for them…how you pitch each might be a little different.

I can’t overstate the fact that relationships matter. You can’t start this process with 3 months of cash. You should be thinking about this even if you plan to conquer the world — get to know key decision makers/GMs at every potential acquirer because…you never know.

And again, my approach wasn’t “I want them to buy me.” It genuinely was “I want this *commercial* deal with this company, because it will be transformative for MY business.” Which was 100% true.

There’s also the reality that sometimes your current “business” scale makes your “product” less appetizing (what does the acquirer do with all the people/processes if they want to repurpose?). This is the hardest part: do you change your business to make it more palatable?

GENERALLY, the answer is NO. Most M&A fails. Again, when you want to sell usually does not align with when they want to buy. But if you really NEED to sell, it’s useful to think through the “anchors” holding you back: https://x.com/arampell/status/1562557849128931328

“Running a process” to sell a company rarely works if selling team or product, especially when product needs to be repurposed…but if you are already being hotly pursued, then and only then (IMHO) does it make sense to “shop” — “Boy who cried wolf” syndrome is real.

Because again, “when they want to buy” is a real thing — maybe they just bought a giant company and don’t have the budget/fortitude to buy another one. Maybe they whiffed their last quarter’s earnings. Don’t push a string. Hurts your chances when they’re ready to buy.

Sometimes you can help expedite, though: once you already have the relationships, and ideally some product integration in place, you can, say, start a fundraise and ask if they’d like to invest (might make acquisition more expensive down the road, maybe they should buy now!)

In the absence of competition, though, it’s very hard to speed up an in-flight M&A conversation/process. And it WILL suck up most of your time and energy…and distract every member of the team working on it. Limit the circle of knowledge on this — it’s crucial.

“Raise money when you don’t need it” is the normal advice for fundraising. For M&A, I would strongly encourage everyone: “Build relationships and think about this…when you don’t need to sell.” Because one day…you might want to or need to.

And again, this doesn’t mean CEOs should spend most of their time on this. I think ideally it’s 5-10% just focused on capital raising/relationships (inclusive of prospective M&A) as a background process.

Lastly, if you want a good price — much less likely when your growth has stalled. The best (luckiest?) deals I’ve seen done are when the CEO (recognizing an upcoming speedbump) basically “expedites” interest…and when the “wants to sell” and “wants to buy” variables meet 🙂

Originally posted as a Twitter thread on December 08, 2022

“The Goldilocks Zone of Cost Irrelevance”

Some of the most valuable companies provide a crucial service, but don’t charge enough to have customers care enough to switch/think about switching

Janitorial services, payroll services, etc. Hard to be displaced / hard to get in.

At TrialPay I called this the “Janitorial Services Problem” — imagine writing a BigCo CEO: “I will make your toilets 19% cleaner for 7% less cost!”

CEO likely won’t care or even care enough to *find the person who DOES care*

It’s actually possible nobody does!

There really is a Goldilocks Zone here. If you represent a giant cost, it’s worth optimizing/RFPing. If you’re too cheap you likely can’t afford a sales team to sell in. But if you’re “just right” — irrelevant to COGS, but you have high margins and a large n of customers…wow

For many of our clients we were a small % of their revenue. Nice, but not crucial. Unlike janitorial services (which every office needs), we were doing something new — so category creation in a zone of irrelevance (eventually it became a category, though)

Moreover, put yourself in the shoes of the CEO…who likely only cares about 1-3 BIG things/KPIs that will move revenue, profits, stock price, save their job, secure their bonus, etc

So if you have a “janitorial services” type product — hard to get in, hard to displace, not incredibly relevant — how do you start? Some things we tried to do…

If leading with your product — do not just try to “go high” — selling to the CEO, board, whatever. They likely will not care! They will not care to find the person who cares! This is a rookie mistake I see many entrepreneurs make.

HOWEVER, if you do get a high level connection, try to lead with something they care about, and link it to your service. I would always try to figure the key priorities of the company and try to lead with that, versus “we’ll make/save you some small incremental dollars”

As an example, they might have (strategically) cared about showing they were ramping up Facebook customer acquisition (in 2011). Or mobile. Optics — if linked to a “braggable” KPI — almost always trump small dollars.

One other clever thing we did was use a bundled hook, as I called it. BigCo CEO didn’t care about our product, but did care about supporting Charity XYZ — so it was a much better reach out to say “we are working on something to support XYZ…”

We did a promotion called “The BigBundle” where 100% of proceeds benefited the American Cancer Society. We kept nothing, not even payment fees. The bundle consisted of…products from our merchant customers that we would sell to consumers.

It turned out to be a pretty clever hook — doing well by doing good — to get more companies to use us. In order to include their product, they needed to sign a contract with us, integrate some code (so we could deliver/authorize), etc.

I often described a customer journey as 10 stages.

Stage 1: Who the hell are you? Go away

…

Stage 6: Contract signed

Stage 7: Code integration complete

Stage 8: Small test done

…

Stage 10: Fully live and turned on, key integrations done

The “BigBundle” got us to Stage 7 with several dozen NEW customers — which then made it really easy to solve the Janitorial Services Problem in the future

After finishing the charitable promo, we had signed contracts and live integrations — so now the sales pitch was so much easier. “Just reply ‘yes’ and the toilets will automatically get 19% cleaner at 7% less cost — we’re already integrated and past procurement”

And once we were the new Janitorial Services Company, we could defend our position quite nicely — knowing how hard it was to get in 🙂

Inspired by a morning conversation with @davidu and @martin_casado — thanks guys!

Originally posted as a Twitter thread on October 25, 2022

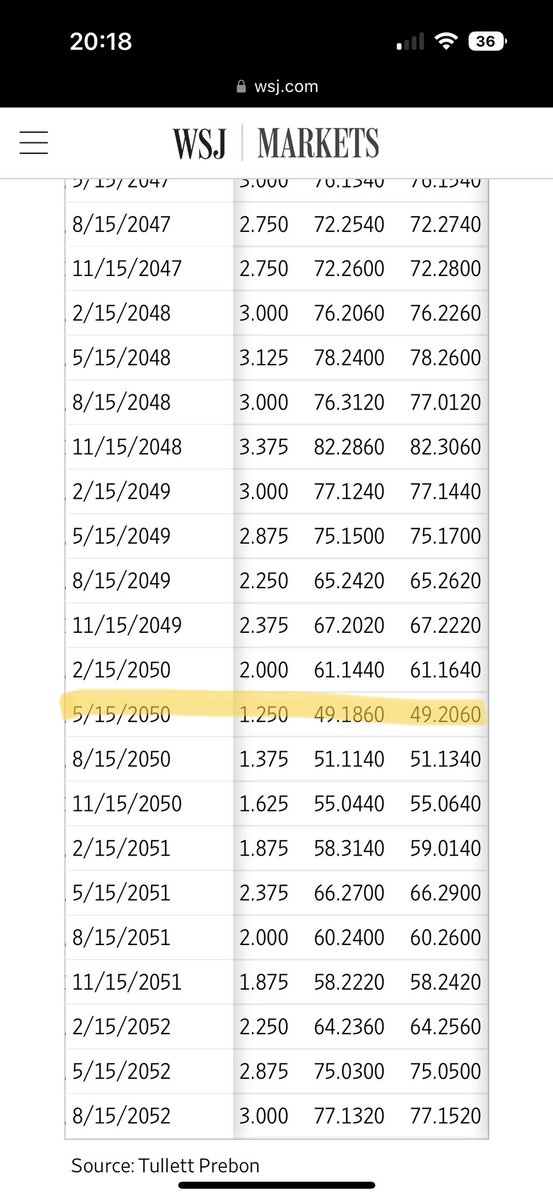

If you had bought the May 2020 30 Year T-Bill (1.25% Coupon) at auction, you’d currently be holding something worth LESS THAN $.50 on the dollar. The Aug ‘22 issue is trading at $.77!

If you are investing your cash, no matter how safe the instrument, MATURITY MATTERS.

I know Fintwit knows this. But if you are, say, an unprofitable startup investing your cash, *do not invest in long-maturity products* — it doesn’t matter how safe they are. Holding to maturity is not the benefit it seems. And the problems are magnified with illiquidity.

Originally posted as a Twitter thread on October 17, 2022

How we almost merged our company TrialPay, many times, while navigating the “can’t raise cash without growth, can’t grow without raising cash” problem. The embedded thread shows the surviving path, but let me walk you through several that *didn’t* work https://x.com/arampell/status/1562557849128931328

It’s not uncommon during bull markets to have too many competitors on the field for a given space. A “roll-up” can theoretically create more pricing power while eliminating redundant teams, tech platforms, etc…increasing revenue while lowering OpEx! “Synergies” galore 🏦💵

And even without an “over-competed” space, you might have one company with LOTS of cash, and another with lots of product-market fit but unable to raise…so one way to “raise money” is effectively to just merge with a cash-rich competitor. If cash is king, merge with cash!

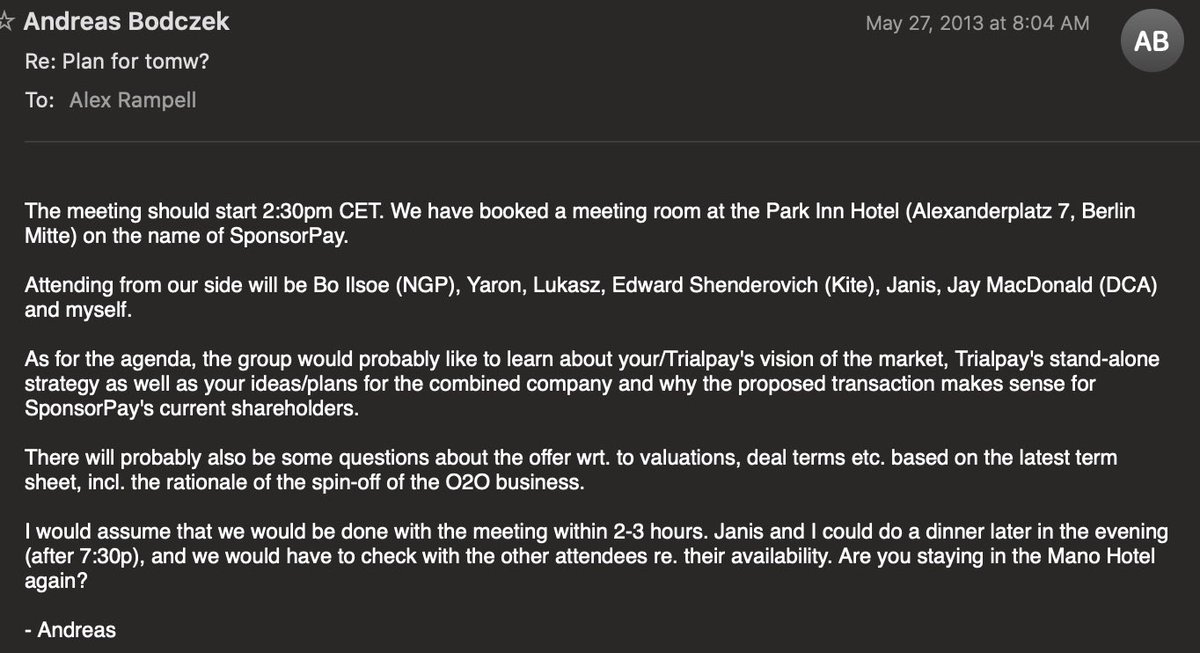

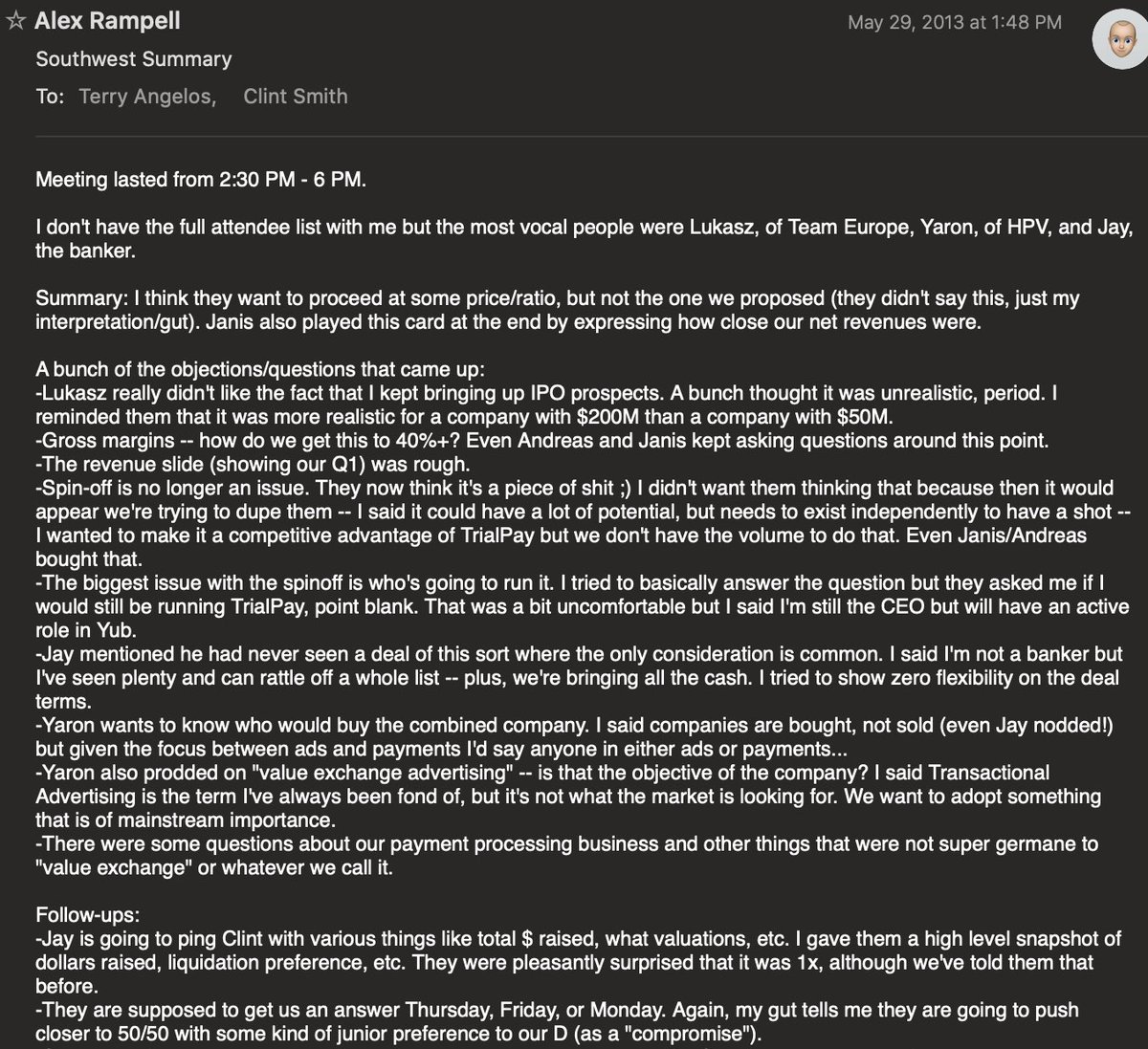

Let’s go back to May 28, 2013. Here I am in the *last* row of the now defunct AirBerlin, flying from LAX to Berlin to meet with SponsorPay regarding a merger. I needed to make a presentation and proposal, which I attempted to do from my seat…despite the reclining guy in front

The problem with private-private mergers is obvious. How do you ascribe relative value to each company? For public companies, there’s a constant voting machine. For private companies, you have an old valuation, cash in bank, burn/revenue, and rosy projections around the future

We had just come off another merger that was almost magical. We bought a company called Lift Media with an identical product, moved all their customers to our platform, only needed one person from their team (not to sound heartless)…so we got all their revenue w/ $0 cost

With SponsorPay, we had more cash and more revenue. We were (internally) bearish on our future growth, since we were late to mobile. They were more bullish on their future growth. We both were probably showing a bit more bravado during the negotiations – my opening slide here

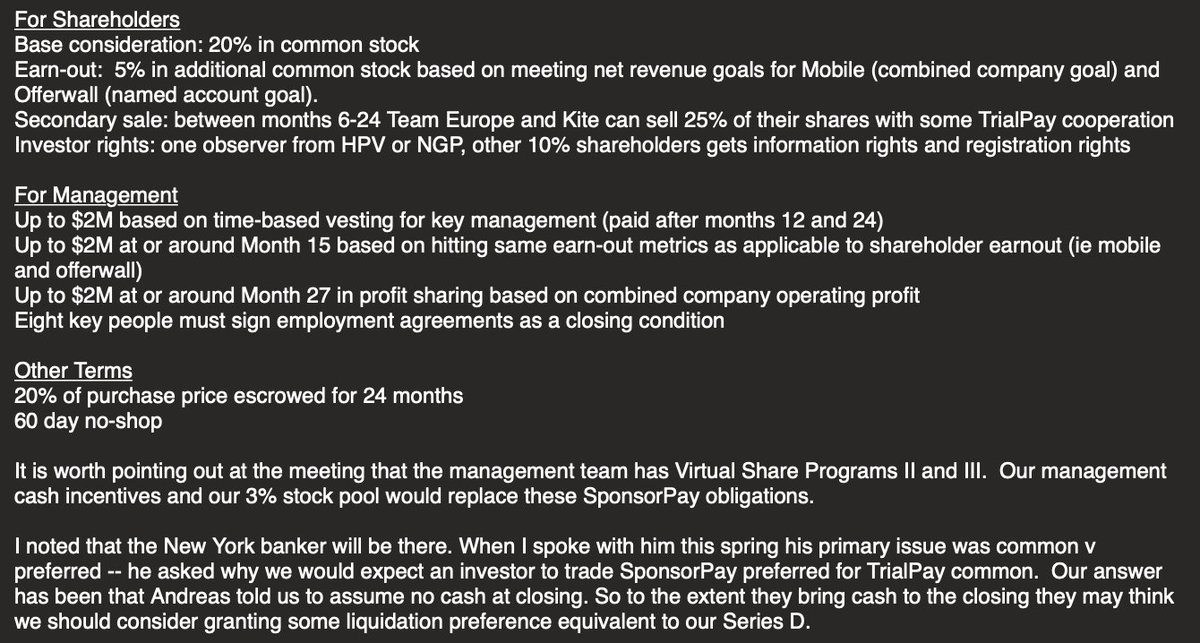

After looking at their financials and our relative cash positions, here’s what we offered (I figure the statute of limitations is up on sharing this stuff since neither company exists anymore! SponsorPay became Fyber became Digital Turbine, so you know how the story ends)

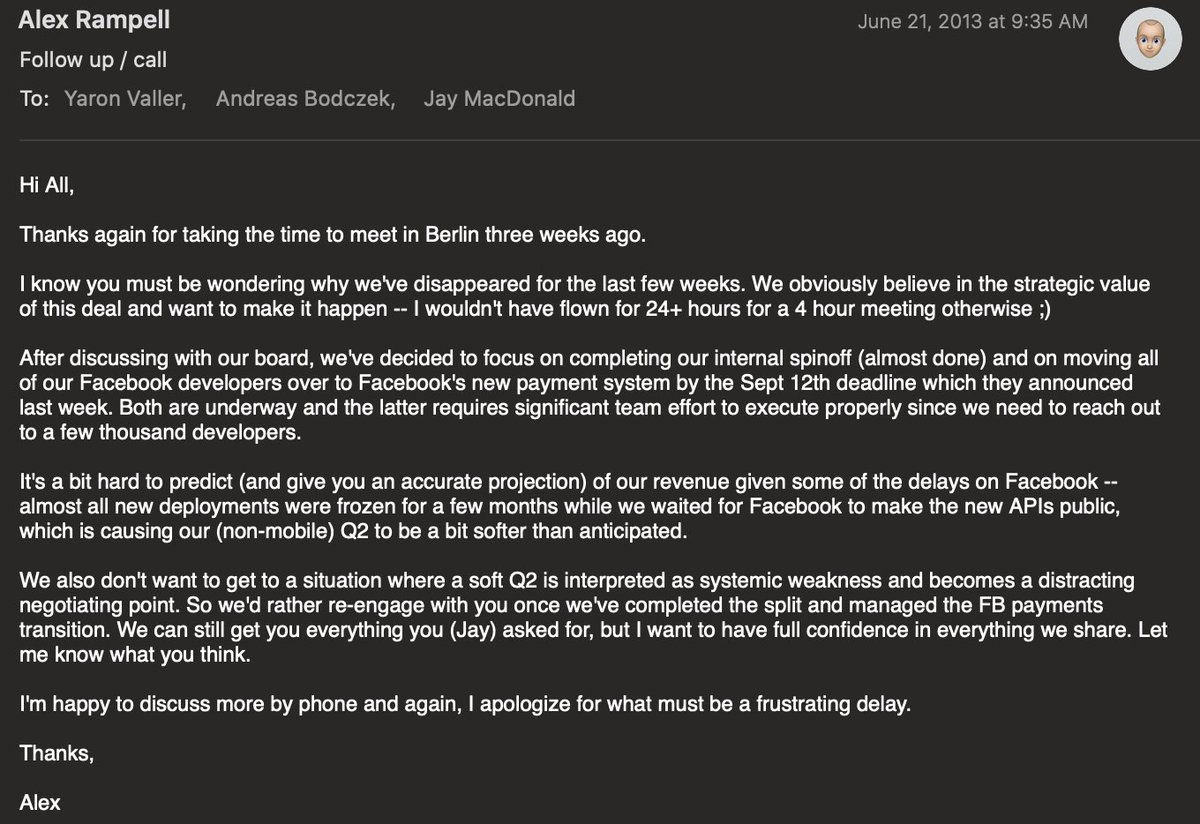

But it was a hard sell. Their investors wanted cash, or at the very least not common stock in our company. We were busy with our spinoff of Yub (see thread in 1). They had hired a banker to try to “shop” our deal. We basically got nowhere, but we didn’t have a sense of urgency

We were also very torn on further diluting our ownership to “double down” on our core strategy by doing a competitive merger. Did it really make sense to give up 20%+ to get more revenue scale but still have 10 other competitors? Like whack-a-mole…with the smallest mole.

I was honest with them that we were busy on our spinoff and likely to see some short term financial pain, and didn’t want to enter the negotiation on “defense” as a result of this. But honestly, my biggest concern was the adage that two turkeys don’t make an eagle

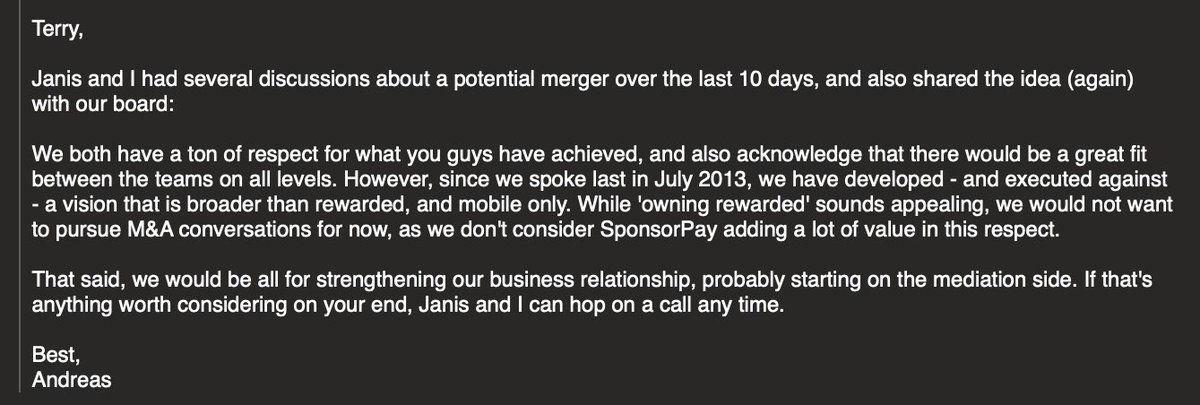

As the year went on, we missed our numbers. They were doing better. We still had more cash. But while we kept opportunistically trying to make this happen, we became further and further apart on price and *strategy*…and after about a year they pulled out, rightfully so.

We were pursuing other deals as well. Accel had a challenged company called GetJar which we looked at buying, but we couldn’t get there. I spent a ton of time with PE firms looking at doing a take-private + merger with a public company, Digital River, that needed new tech

This one (DRIV) was arguably the most insane. Merge our unprofitable company plus tech-forward and differentiated team into a profitable but slow-growing public company, steered by a slash-and-burn PE firm. But valuation was even more challenging in this model.

We prostrated ourself in front of every company adjacent to us but our cash position, once our strong point, was weakening. We even had conversations with “that stock might be valuable!” tech companies (future eagles, with us almost acting as VCs) but we had too much rev/opex

But several learnings from this experience of private-to-private M&A, including when I’ve seen it work well.

A. 🦃+🦃 ≠ 🦅. Make sure there’s a *real strategy* you can get behind

B. Don’t waste time. If you are cash rich in a bad market, that’s your value. Move fast.

C. “Optics” converge on irrelevance quickly. “Optics” are a reason not to cut burn, not to eliminate products, etc. You’re merging with a private company, not a BigCo

D. Roll-ups are good if they get you to market leadership, but not if they leave you with high fragmentation

E. To quote The Godfather II (and Sun-Tzu): “Keep your friends close, but your enemies closer.” Being on good, text-message-banter terms with the CEOs of all your competitors is *always* a good idea…particular in an environment like this.

Hope this was helpful. I think we’ll see a lot more private-to-private deals, particularly amongst late stage companies, in this market cycle. Fin.

Originally posted as a Twitter thread on August 24, 2022

How a company I co-founded (TrialPay) once exited the Catch 22 of “can’t raise cash without growth; can’t grow without raising cash” which is potentially the most “unsolvable” (Kobayashi Maru) situation a VC-backed company can face

First, a refresher. There are basically three outcomes for a VC-backed company:

-go public/get bought

-go out of business

-become a zombie

Let me explain the third one…because you might be thinking “wait, you mean become marginally profitable forever? That’s good!”

Most businesses generate profits + are valued at the present value of those future profits. VC businesses: more valued as call options — “if this thing works, it could be huge!” — which is why a day 0 company with just a PowerPoint presentation is “worth” $50M sometimes

Once things go south, a doom loop can happen:

-best employees don’t believe in the equity and leave

-you need to pay people more to stay, amplifying burn

-customers get nervous

-AND company with immature product can’t (always) cut to profitability…so still burning money

And again, cutting to profitability with almost zero cash cushion might mean never being able to restart growth (esp having lost the best talent in the co), and then the opportunity costs of the founders kick in…why stay? Particularly with albatross of a “stale” cap table

Now to my story re TrialPay. As a payment company servicing digital goods, it was pretty bad when all of the major platforms (eg Facebook, Apple etc) decided to “own” payments. We went from $25M revs (2010)->$70M (‘11)->$77M (‘12)…to $55M (‘13). Not good, esp when market⬆️

Many of our most talented people started leaving. We had gone through M&A conversations with every major strategic buyer and twice been left at the altar — very hard to come back once you have that Scarlet letter. We executed a big RIF, downsized office space, etc…the usual.

But we did three unorthodox things that uniquely turned things around and yielded a 9-figure exit:

A. Promoted aggressively from within

B. Spun-out a company (dividended it out to shareholders) which later had its own exit

C. Sold some of our IP

Promoted from within: companies compensate people with cash, equity, and title/responsibility. We were low on cash, nobody believed in our equity, so we started taking junior people and making them VPs+ — a huge amount of responsibility they wouldn’t and couldn’t get elsewhere

Generally speaking, people want career/title progression, and don’t like leaving a company to take a “lower” job elsewhere…which is a nice realization if you are bleeding talent. Responsibility can really motivate fresh people.

next: Spinning out a company. We did an IRS Section 355 tax free spin out — which basically means we took one product, wrapped it into a new company, mirrored the cap table but flattened preference stack and removed most liq pref, added a new big option pool, and spun it out

This was almost alchemy. On one hand we had people who wanted to stay at the mothership if they had more title/responsibility; on the other were engineers and product people who wanted a true high growth startup again, not a colossal shrinking turnaround

At TrialPay we had this $6M/year project/team to build an “offline affiliate network” using credit card rails which TrialPay could then use for offers (eg “get Zynga coins for free if you shop at Starbucks”). It was a great idea but only yielding cost, no revenue

So this is what we spun out.

But with lower cost because we gave people big equity packages at an exciting new startup with a very low valuation and no preference overhang.

So it was better than zero sum: we reduced burn at TrialPay (costs spun out), implemented more startup-like packages at our spin-out (less cash, more equity — with an easier path to exit for that equity) — so the burn of NewCo was lower than the same team had been at TrialPay

Sure enough, within ~6 months a company (Coupons Inc) bought our spin-out for $30M, and there was lots of interest since it was a lean engineering-centric organization. It wasn’t a home run but everyone (including TrialPay employees, since we mirrored cap table) made money

Many of the would-be acquirers had passed on buying TrialPay since we were losing too much money and were too big with too many things (they wanted us for X, not X + Y + Z). But spinning off a key strategic asset changed that.

Finally, at TrialPay we sold a license to our core software to Visa, an existing investor in the biz. This provided a meaningful amount of cash to TrialPay (we turned a profit that year), further shoring up our balance sheet, and a small team went to Visa to help implement

This gave birth to the Visa Commerce Network, but since it was still reliant on many parts of TrialPay, Visa decided to buy the whole company of TrialPay later that year, ending a daunting 2 year battle of “can’t grow without capital; can’t raise capital without growth”

It was a very trying experience, and I distinctly remember @bhorowitz taking the time (as a non-investor who barely knew me in 2013!) to give my co-founders and me guidance and counsel as we navigated between rocks and hard places. Hope this helps others in the same boat. FIN

“BigCo X offers installment payments on existing payment rails” is not really competition to a wide set of use cases that Buy Now, Pay Later enables, because without allowing the merchant or manufacturer to lower the interest rate or extend the term, it doesn’t change behavior

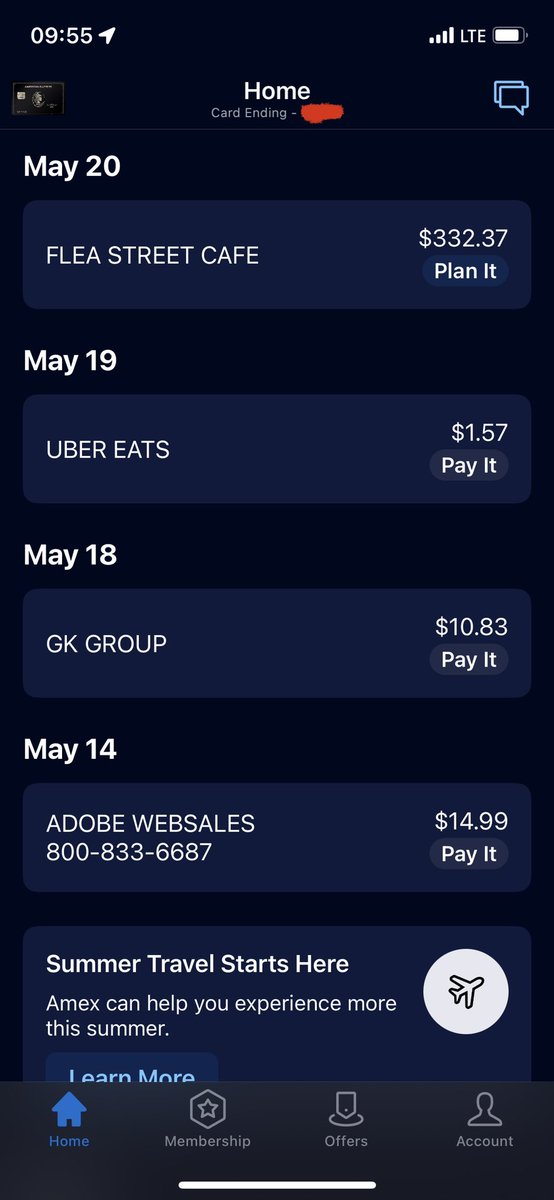

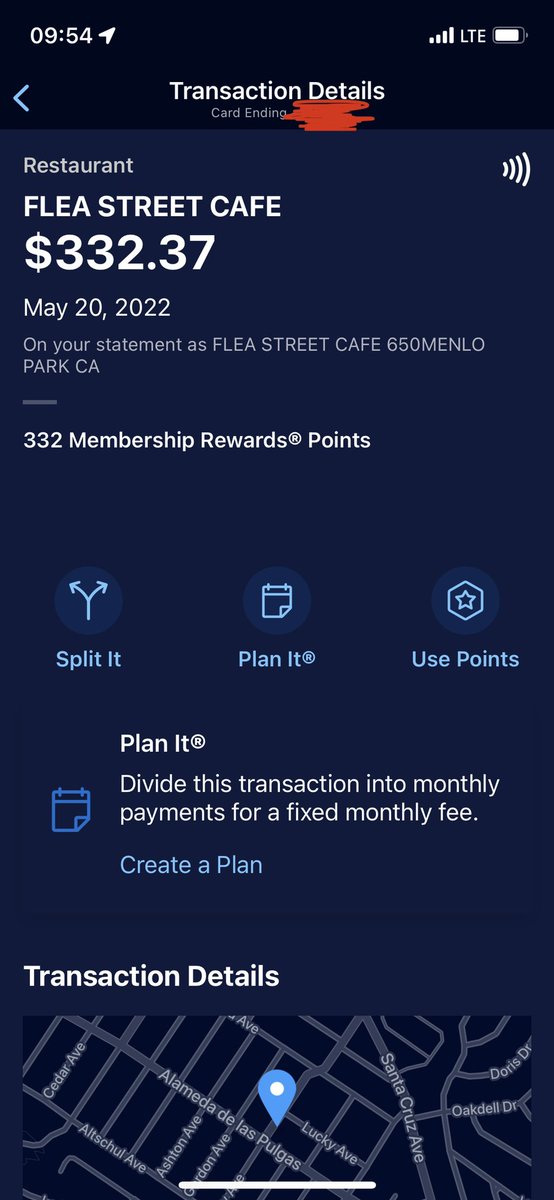

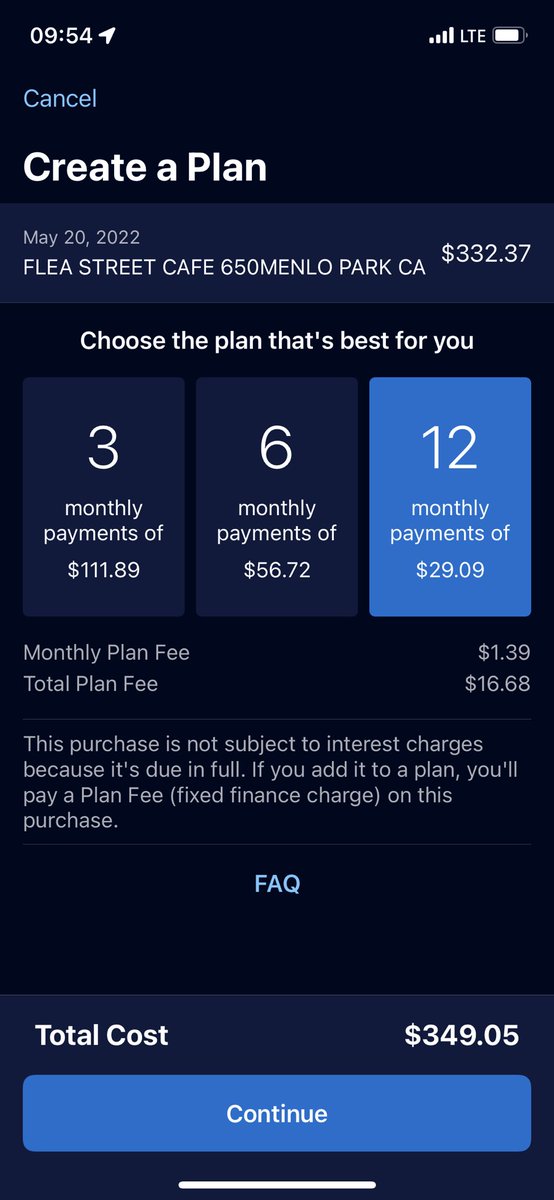

For example, Amex has offered *for a long time* a product called “Plan It” which works great and allows any purchase to be turned into a set of installments.

Here’s my Amex bill

I click on “Plan It” next to my Flea Street payment (great restaurant btw) and can either Split It (with friends, using Venmo or PayPal), Plan It (turn into installments), or even Use Points

I’m going to use Plan It, which offers me several installment plans — 3, 6 or 12 months. No interest but a monthly “plan fee”

This works great, but to the point at the beginning — it misses the fact BNPL is a *promotional tool used by manufacturers and merchants to sell more stuff* — eg, Toyota often offers and *advertises* 0% financing to induce you to buy (promotion!)…not “post payment planning”

ApplePay is awesome, and integrating installments to ApplePay makes sense, just like it made sense for Amex, above. But the “consumer + merchant + manufacturer” magic of BNPL happens when merchants/manufacturers can lower rates and extend terms to consumers…

…and can actually integrate those lower rates and extended terms into promotional materials in order to bring customers TO the checkout. It’s “too late” to first show this in the literal checkout line…which is why car manufacturers have run financing promotions for decades.

BNPL “done right” brings this same set of tools to any merchant and even any manufacturer (see long BNPL thread above on manufacturer-sponsored offers), helping unlock sales that otherwise would not happen

Government and platform (yes, some platforms have that much power) regulators do customers *and* entrepreneurs a favor with smart regulation, because it forces companies to compete on who can do the best job for the *customer*