Originally posted as a Twitter thread on June 07, 2022

“BigCo X offers installment payments on existing payment rails” is not really competition to a wide set of use cases that Buy Now, Pay Later enables, because without allowing the merchant or manufacturer to lower the interest rate or extend the term, it doesn’t change behavior

For example, Amex has offered *for a long time* a product called “Plan It” which works great and allows any purchase to be turned into a set of installments.

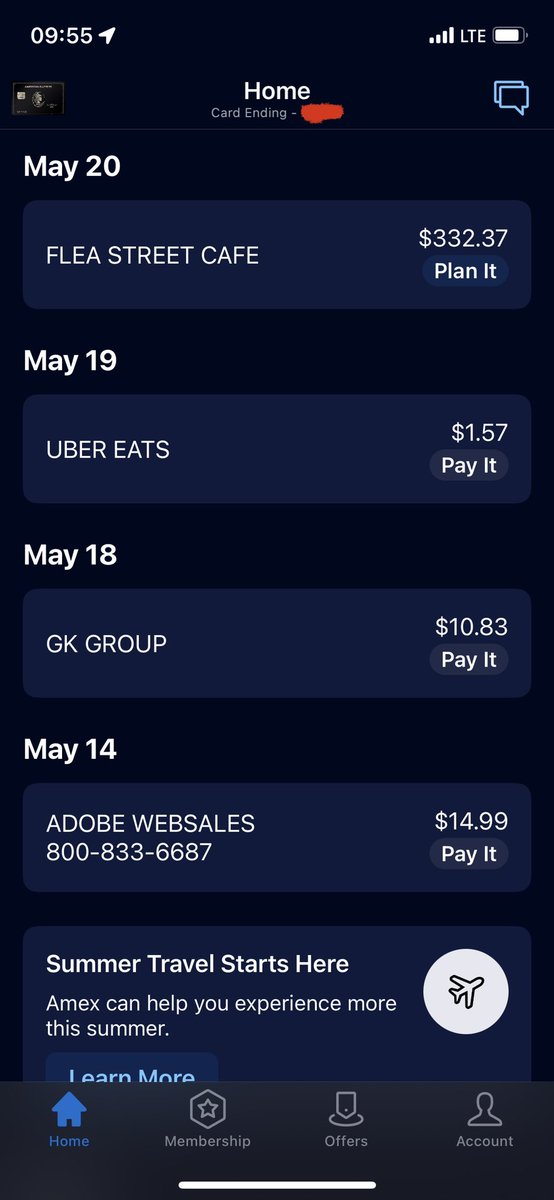

Here’s my Amex bill

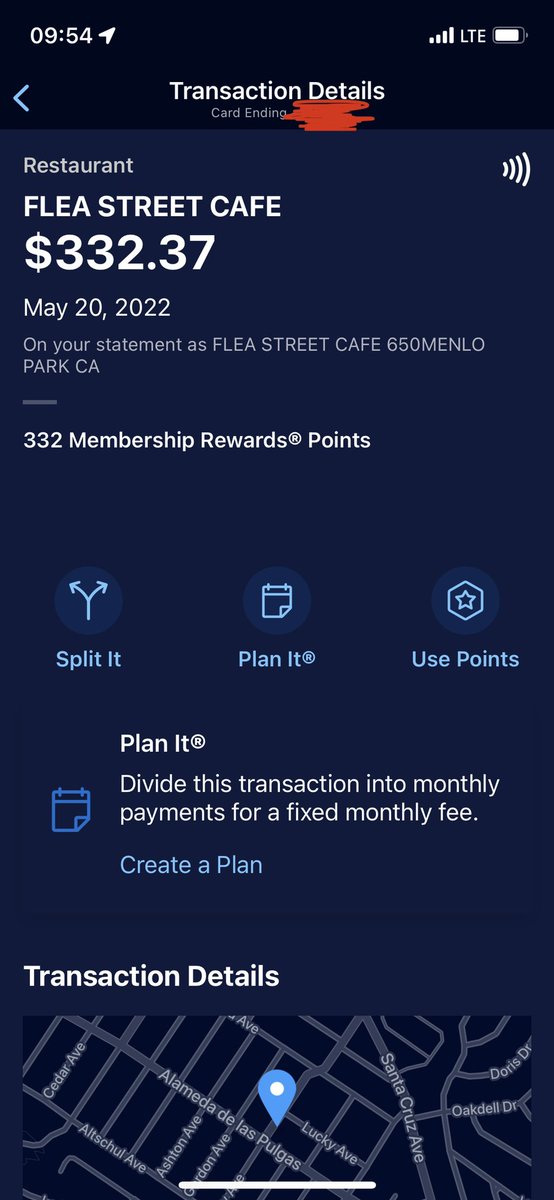

I click on “Plan It” next to my Flea Street payment (great restaurant btw) and can either Split It (with friends, using Venmo or PayPal), Plan It (turn into installments), or even Use Points

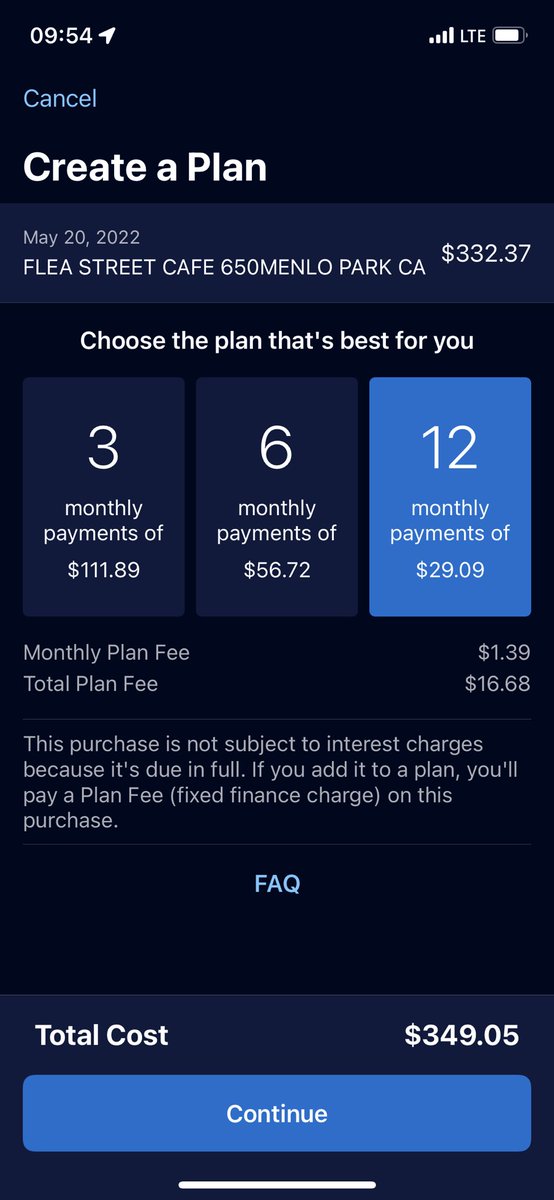

I’m going to use Plan It, which offers me several installment plans — 3, 6 or 12 months. No interest but a monthly “plan fee”

This works great, but to the point at the beginning — it misses the fact BNPL is a *promotional tool used by manufacturers and merchants to sell more stuff* — eg, Toyota often offers and *advertises* 0% financing to induce you to buy (promotion!)…not “post payment planning”

More on this from a thread I wrote in September 2021: https://x.com/arampell/status/1435692945387048964

ApplePay is awesome, and integrating installments to ApplePay makes sense, just like it made sense for Amex, above. But the “consumer + merchant + manufacturer” magic of BNPL happens when merchants/manufacturers can lower rates and extend terms to consumers…

…and can actually integrate those lower rates and extended terms into promotional materials in order to bring customers TO the checkout. It’s “too late” to first show this in the literal checkout line…which is why car manufacturers have run financing promotions for decades.

BNPL “done right” brings this same set of tools to any merchant and even any manufacturer (see long BNPL thread above on manufacturer-sponsored offers), helping unlock sales that otherwise would not happen